Mike Alford the CEO of Alaric International believes that this trend points the way for many Western economies. However, corresponsal banking organisations now have rigorous demands for the payment systems required to support such an increasing range of services. With Alaric’s Authentic payment system already meeting these criteria with Central American retailer Grupo Sanborns, he draws on his own company’s experience to explain the benefits and demands of this retail based form banking service provision.

Unbanked Populations and Market Challenges

Taking Mexico as just one example, there is a large unbanked population, with just 25 million bank account holders out of a total population of 120 million. Thus, with the proliferation of mobile phone usage (in total some 70 million handsets in Mexico) cell companies are vying to offer mobile banking services and to encourage their clients to become banked.

In addition, the banking infrastructure is predominantly urban in all the region’s countries. Mexico is no exception. Consequently, there is little in the way of a traditional branch network in remote locations or in those areas with difficult terrain. With only about 150 branches per million population in Mexico compared to nearer 400 or more in countries like the United States, Germany or France, the limited branch network is a serious handicap in reducing the unbanked population. With the Mexican government’s active encouragement, this has given rise to the concept of ‘corresponsal banking’.

How Corresponsal Banking Works

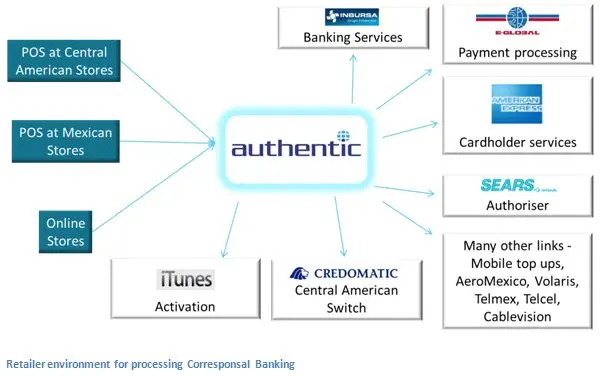

Corresponsal banking enables retailers with a wide geographic presence to have a correspondent relationship with one or more banks and therein to enable their clientele to perform a range of banking transactions in-store at the point-of-sale.At the most fundamental level,this delivers services such as balance enquiries, transfers, bill payments and also withdrawals. And it is important to note that these are account based banking services and not just an extension of the standard card transactions.

It has proved be a very popular development and as a result there has been significant growth in the provision of these retail based banking services. Many people prefer to withdraw money in-store rather than from a street-side ATM due to concerns about the risks of mugging and other criminal activity in exposed external locations. The long opening hours (for instance 7am to midnight) and weekend opening of the retail stores allows people to access their funds day and night, within the comfort and security of their local store.

Range of In-Store Financial Services

Another noticeable sign of the success of this approach is the proliferation of services now available in-store. Some of these services are standard banking functions such as withdraw cash, pay in cash, cash cheques, transfer funds between accounts or get an account balance. But they are extended with a large range of functions. Bill payment services such the payment of credit card bills, loan installments, utility bills and insurance premiums are common. And some specific functions are also available such as the purchase of mobile phone top ups or paying for airline tickets. So the retail store is providing the full gamut of banking services a consumer would expect to find in a bank branch.

The challenge for retailers like Sanborns is the need to handle traditional card based shopping transactions that will be authorised through the mainstream card processing channels, the retailer gift card or store card purchases which will be managed by the retailer themselves or a processor acting on their behalf and these more complex banking payments which need to be channelled to the specific bank involved.

Benefits for Banks and Retailers

For the banks involved, extending their reach through partnerships with retailers allows them to grow their customer base without the significant cost of creating bank branches. The major retail chains have typically thousands of outlets, a network that would be unachievable for any bank. So the fees payable to the retail chain are a financially viable route to enabling wide access to the bank’s services. The bank still needs to ensure its products and services are promoted in all regions to drive new customers. And as these previously unbanked consumers become comfortable with making use of the banking system, there is the opportunity to engage with them through phone or internet banking or, more likely, mobile banking.

Future Outlook for Corresponsal Banking

With the availability of systems capable of being deployed in-house to support the increasing sophistication of corresponsal banking, the chances are that its spread will continue. It is also fair to say that whilst the populations of Central and Latin American may remain relatively unbanked in the traditional sense, the facilities offered in such countries will continue to be more advanced than those in some other Western countries.