By: Rajashekhara V MaiyaAssociate Vice President & Lead Product Manager-Finacle Product Strategy at Infosys Limited

Retail banks continue to focus on innovation…

While the results of the 4th edition of the annual study on innovation in retail banking, presented by Efma and Infosys, largely mirror those of the previous surveys, they also differ in subtle, yet significant ways. For instance, in the 2nd edition of this study, 61% of surveyed banks said that they had invested more in innovation compared to the previous year, compared to 11% who had done just the opposite. Two years later and in the midst of a challenging environment, 73% of the 300 bankers surveyed confirm increasing innovation investment compared to 2011, whereas just 6% say they have scaled it down. Also, while European respondents continue to assess their innovation performance rather pessimistically, this year a little over half concede that they have become more innovative. Other differences observed in the 2012 survey include a growing threat perception from disruptive innovation, owing no doubt to the entry of non-banking players from the telecom, retailing and technology space, and an increasing use of open innovation by banks. For example, Barclaycard’s crowd-sourced credit card and ING Bank’s customer experience center were both built through open innovation.

Retail Banking’s Commitment to Innovation

The findings of the 2012 study indicate that retail banks worldwide are now firmly committed to innovation. And while innovation understandably plays second fiddle to risk, balance sheet and cost management, 79% of banks acknowledge that it is strategically important to the future of their business. They are also quite certain of its direction, which is clearly towards channels, customer service and experience.

…to drive customer acquisition and revenue

In the 2009-2011 surveys, respondents said that innovation was critical to both growth and efficiency, perhaps somewhat more to the latter. The latest study marks a shift in thinking, because for the first time, customer acquisition and revenue growth clearly outrank cost efficiency and compliance as the key drivers of innovation, in all the four regions, namely, Europe, Middle East and Africa, Asia Pacific and the Americas. 75% of respondents are increasing investment in channel and customer service innovation in order to achieve these goals. Region-wise, European banks appear to be the least enthusiastic about investing in channel innovation, reporting only a net balance of 59% (proportion of banks increasing investment minus those decreasing investment). All the other regions report a greater than 70% figure, with Middle East and Africa leading the way with 89%.

Digital Channels as Innovation Frontiers

Channels, especially online and mobile, are a top innovation priority

The choice of channel comes as no surprise: nearly 2 out of 3 banks say they are highly innovative in the online channel, whereas more than half say the same about mobile. What is somewhat surprising is that although 87% of banks concur that IT is important (or very important) to channel innovation, the branch channel continues to consume more of the IT budget than any other; however its share is lower than that of online and mobile combined.

Online Banking and Personal Finance Tools

Personal Financial Management tools are the most popular innovation in the online channel; 29% of banks have already introduced them, and another 60% are planning to do so within 3 years. Social media is another area of interest and around 1 in 4 banks have integrated some services with Facebook and other sites. ICICI Bank, India’s largest private sector bank offers a Facebook banking service providing account information, promotions etc., which links back to the bank’s website; it is the first Indian bank to provide more than just marketing information through social media. Interactive options like web chat or click to call, designed to improve customer experience, are also catching on; 1 in 5 banks surveyed have them already and almost all of them will do so in the next 3 years. This intent is clearly visible in Alior Sync, a new service from Poland’s Alior Bank, which it deems the world’s first virtual bank providing videoconferencing access to staff as well as documents and desktop sharing.

Mobile Innovations and Augmented Reality

The list of mobile-related innovations features advanced visualization and mobile payments at the top. The first – better known as augmented reality – is on offer at 38% of banks in the form of branch and ATM locating services; a comparable number of banks facilitate the second through contactless and P2P payments and mobile commerce. On the other hand, personalized location-based offers and mobile wealth and advisory services are yet to take off, and will take about 3 years to catch up with some of the more popular mobile innovations.

With regards to channel strategy, 86% of banks said that multi-channel integration was important, followed by 81% for the single customer view and 72% for multi-channel analytics. These capabilities are critical and complement innovation to deliver a superior customer experience.

But action on the ground does not match intent

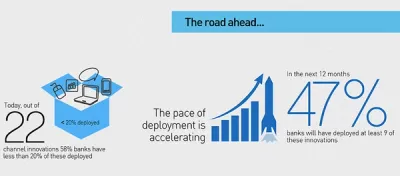

However, the above expectations are tempered by other, less optimistic findings. Arguably, the most significant one is that even today, only 2 in 5 banks have the structure and metrics to measure their innovation performance. Next, the enthusiasm for channel innovation is belied by poor adoption – as per the survey, nearly 60% of banks have deployed less than a fifth of the 22 channel innovations that are listed. Fortunately, the speed of adoption is picking up, and it is expected that nearly half the banks will have deployed nearly half these innovations in a year’s time.

Regional Differences in Retail Banking Innovation

No two regions are the same

In Europe, where innovation is the fifth priority after risk and cost management and others, the online channel draws the highest share of IT investment, which is consistent with the region’s high Internet penetration, led by the countries in North Europe.

For banks in the Middle East and Africa, the mobile channel is clearly where the focus of investment lies, which is understandable given its role in building financial inclusion in countries with poor banking penetration. Although banks are upbeat about their innovation performance, they seem to have achieved it with an informal approach; relatively, fewer banks in this region have a formal innovation structure.

Asia, with its diversity, faces a wider variety of innovation issues and challenges. Surprisingly, banks rate innovation in the online channel ahead of that in mobile. At the same time, they are keen on attracting the large, young population of their countries with new, high technology innovations.

American banks have a different priority to the rest. For them, customer service and customer experience innovation takes precedence over channel innovation. Within the latter, the online channel is considered more important than the branch or mobile.

Financial Inclusion through Innovative Channels

Financial inclusion is a goal for some

Although the attitude and approach to innovation is consistent across regions, banks from the developing world have an additional responsibility to promote financial inclusion in their markets. Here, mobile channel innovation is offering able support – and sometimes even leading – traditional inclusion models leveraging banking correspondents, agents and microfinance institutions.

In India, Eko, a correspondent of the State Bank of India and ICICI Bank serves nearly 1 million customers through a low cost distribution and payment channel comprising over 1,300 small retail outlets offering no-frills bank accounts and basic financial services. Agents and customers transact with core banking systems using mobile text messaging.

Ghana’s Ecobank was awarded African Banker’s 2011 “Microfinance Project of the Year Award” for its financial inclusion platform. A multi-channel branchless model comprising 185 agents, 100 ATMs, POS terminals and SMS banking serves over 60,000 customers.

Conclusion

The 2012 study shows that banks worldwide have a similar, positive attitude to innovation, which they are backing up with higher investment, better performance and a clear focus on online and mobile channels.