Banking

May the Best Bank Win: How to Deliver Seamless Digital Experiences to Drive a Competitive Edge

Published by maria gbaf

Posted on January 26, 2022

4 min readLast updated: January 28, 2026

Add as preferred source on Google

Published by maria gbaf

Posted on January 26, 2022

4 min readLast updated: January 28, 2026

Add as preferred source on GoogleBanks must enhance digital experiences using API-led integration and open banking to stay competitive and unlock new revenue streams.

By Jerome Bugnet, Director, Solution Engineering, MuleSoft

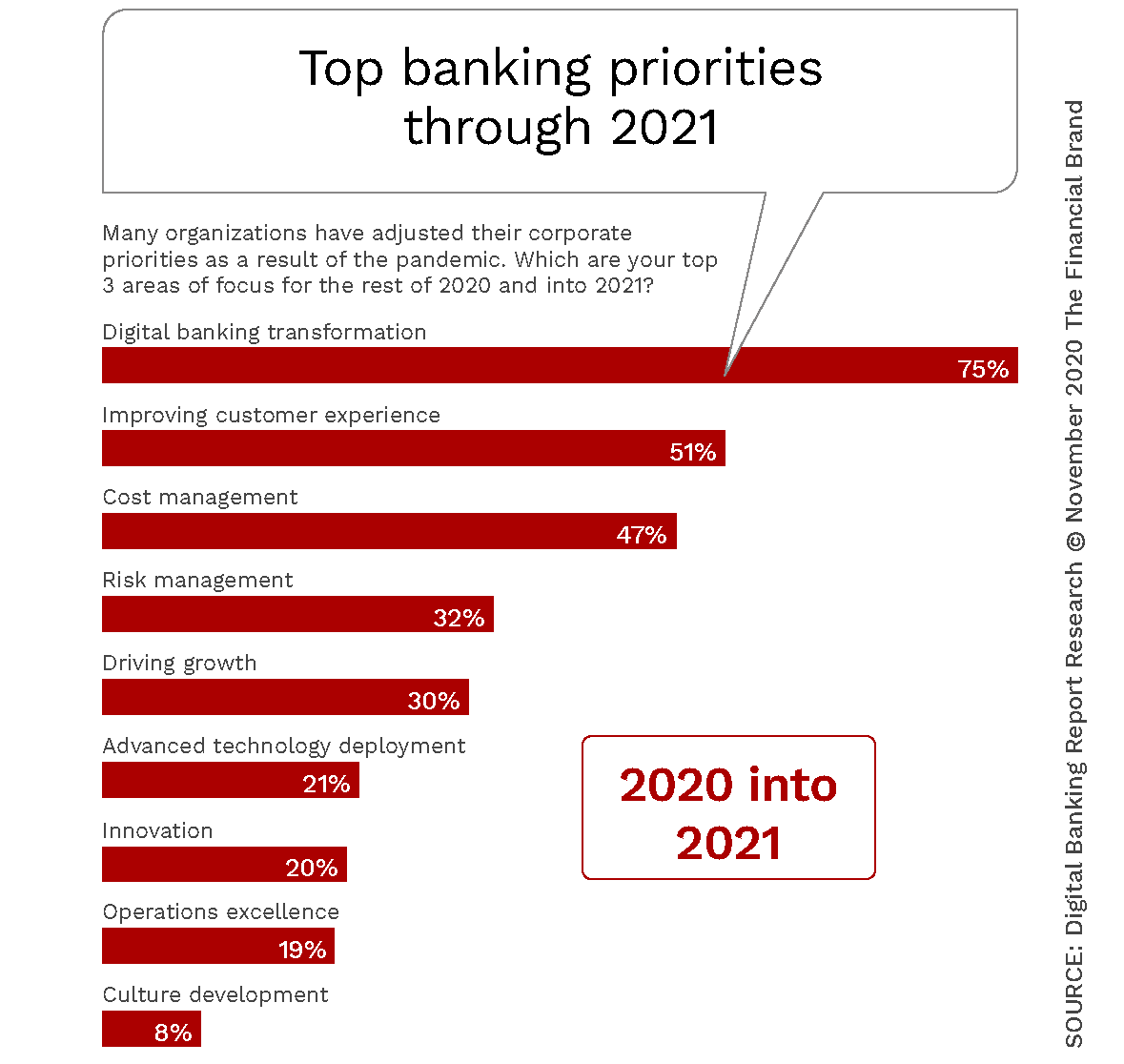

The battle to capture customer hearts and minds is never-ending within the financial services industry, as banks constantly look to increase their market share. According to the Digital Banking Report, improving the customer experience has become a top priority for banks, as they continue to realise its importance to their future success. To compete in this new battleground, there’s a greater need than ever for banks to accelerate their transformation and improve their ability to deliver more seamless digital experiences. However, this is often difficult for banks that rely heavily on legacy IT environments, and calls for a fundamental rethink of how their operating models work.

Devising a battle plan

Banks must first draw up a strategy that will enable a ‘digital-ready culture,’ defined by a willingness to invest in new service delivery models to meet the evolving needs of their customers. This should include a big focus on automation, to make customer experience as frictionless as possible. With innovations such as straight-through loans processing and AI-enabled chatbots, banks can enable greater accessibility and convenience in the way customers interact with financial service providers.

The principles of open banking are also becoming more important, as organisations increasingly see the value in embracing platform-based business models. These models allow banks to collaborate more freely with other service providers to deliver more seamless digital experiences. For instance, they could enable customers to access a mortgage capability directly through a property platform’s app or website when buying a house, rather than needing to approach the bank separately.

Leading the charge

Realising these ambitions is a significant challenge for more established banks. The reality is their IT operating models aren’t typically geared towards customer experience innovation or third-party collaboration. Data resides across multiple silos, making it difficult to access and share freely to improve customer journeys and collaborate with other service providers. Banks’ ability to connect these data silos, along with third party information, and make it more accessible, is key to better understanding and meeting the needs of their customers, both directly, and in partnership with others.

To overcome these barriers, banks should make themselves more composable, by embracing API-led integration to expose data and digital capabilities for others to consume and deliver as part of their own service. With this approach, organisations replace rigid custom code with a flexible integration layer that seamlessly connects together all devices, data sources, and applications. By placing an API in front of systems and data sources, it is much easier to use those capabilities in future integration projects. Becoming a composable business also helps banks accelerate customer experience innovation, by allowing them to see their digital assets as a network of reusable business capabilities. This means both experienced developers and business technologists – employees outside of the IT department – can use existing capabilities to build new digital banking services, without having to start from scratch or write any code. It also makes it easier for third parties to quickly add the bank’s capabilities to their own products by plugging in the relevant API. This uncovers new opportunities for banks to increase their revenue, by joining new value chains.

Pushing the advantage

By taking an API-led approach, not only can banks create more seamless customer experiences, but they can defend themselves from intensifying competition by unlocking new revenue streams and scaling their services into new markets. Crown Agents Bank, a UK based provider of foreign exchange and cross-border payment services, has seen these benefits first-hand, having embraced an API-led integration strategy to support a rapidly growing customer base. The bank previously relied on custom code connections between its front-end services and core banking systems, but found these too rigid and unable to scale. Crown Agents Bank adopted APIs to become more composable, so it could seamlessly connect with its fintech partners and handle a greater number of transactions. It’s since gone from being able to process 1,500 transactions a day to 50,000, increasing its payment processing capacity by more than 3,000%.

In the race to drive a stronger competitive edge, we’ll soon see many other banks following in the footsteps of Crown Agents Bank and embracing a composable enterprise strategy, fuelled by API-led integration. This approach will be key to enabling the seamless digital banking experiences that customers expect. To enable this, banks need to make APIs a strategic focus, to drive greater agility, improved customer interactions, and a digital-ready mindset. It’s this approach that will set banks ahead of their rivals and ensure they win in the customer experience battle.

The article discusses how banks can deliver seamless digital experiences to gain a competitive edge.

By adopting API-led integration and open banking to enhance service delivery and collaboration.

Banks often struggle with legacy IT systems and data silos that hinder seamless customer experiences.

Explore more articles in the Banking category

{kind=link}