Technology

Digital Identities: The Innovation of the Decade?

Published by Jessica Weisman-Pitts

Posted on July 11, 2022

5 min readLast updated: February 5, 2026

Add as preferred source on Google

Published by Jessica Weisman-Pitts

Posted on July 11, 2022

5 min readLast updated: February 5, 2026

Add as preferred source on GoogleBy Matthew Peake, Global Director of Public Policy, Onfido

Before the digital economy transformed how consumers interact with products and services, the way businesses managed and verified their customers’ identities remained relatively stagnant. For many organisations, the default process was to ask a user to show a physical document like a paper ID, or to input a unique passcode. This was particularly the case in banking, travelling and even voting.

Over time, companies sought alternatives to verify customer identities online for user convenience. One method was using Knowledge-Based Authentication (KBA) to verify identities in a virtual space. Powered by Credit Bureaus, this requires consumers to answer ‘secret questions’ about themselves and their financial history that only the legitimate person would supposedly know. However, this is often a lengthy process and is a cause of user frustration. Further, as fraudster tactics evolved and data breaches became more prolific, these systems became direct targets for bad actors because of the volume of information and data they hold.

But as the last couple of years has seen a decisive shift to online services, what started as a mission for convenience is now a necessity that aligns with a long-term behavioural pattern. In fact, one in two now feel more comfortable with online services than they did before the pandemic. So, as businesses pivot to meet their users online, it’s a financial, reputational, and in some cases regulatory obligation that they can accurately and securely verify their customers. This is where digital identity innovation can act as the bridge between the physical and virtual worlds, provide protection against identity fraud and onboard customers quickly and seamlessly.

The value of digital identities has been clearer than ever over the past two years, helping businesses onboard new customers efficiently as the digital economy expanded. But that’s not the only reason.

Today’s fraud landscape is evolving fast. As consumers have moved online, malicious actors have closely followed. So much so that identity fraud has risen 44% since 2019, while the level of organised crime has jumped too with enhanced tactics like 2D/3D masks, deepfakes and replay attacks all being deployed. As a result, users are increasingly aware of their online presence and the value of their personal data. In fact, recent studies show that 57% of consumers now fear their identity is available for purchase online. As a consequence, many are taking a no-nonsense approach to fraud, particularly in the banking and finance sector. More than 40% of banking customers, for instance, said they would immediately close their account or switch provider if it was compromised by fraud.

This shows that the stakes are higher than ever for online businesses: fail to verify customer identities and they could be hacked, leave their users exposed to fraudsters, lose revenue and ultimately dismantle the trust they’ve built. Over the next decade, digital identities will be crucial so that businesses can stay one step ahead of increasingly sophisticated fraudsters.

Setting a new standard for virtual identities

But how do they do this? Today, digital identities are grounded in emerging, innovative technologies that are designed to mitigate fraud attacks.

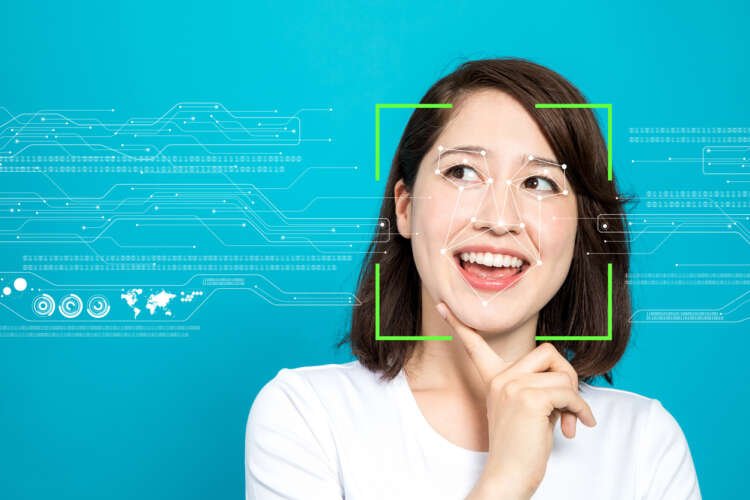

Machine learning and biometrics play a critical role in the digital identity verification process. They enable users to verify their identity simply by taking a photo of their ID and posting a selfie. This confirms they are the legitimate ID owner and are physically present. Unlike traditional KBA processes, this protects against identity theft and impersonation, and significantly reduces the potential for identity fraud.

Beyond this, digital identities are now paired with advanced innovation like AI and low-code solutions to power best practice in fraud prevention. For instance, AI is automating the entire identity verification process, allowing businesses to select ‘pass’ requirements based on risk, and complete checks in under 10 seconds. This means that businesses can layer the security behind their onboarding checks for high-value or riskier services, like mortgage applications and loans, without impacting the overall customer experience.

While low and no-code solutions are making it easier than ever for businesses to implement digital identities. With improved accessibility, all businesses can access powerful analytics and make intelligent, real-time decisions on the onboarding process – staying one step ahead of fraudsters and protecting users.

The decade ahead

Early adopters are already seeing the benefits of this new and improved standard of identity verification. Today’s sophisticated fraudsters have closely followed consumers online and it’s no longer enough to combat this threat by asking users to input a unique passcode or to show a physical ID document to prove their identity. Those that do risk reputational damage, loss of revenue and a breakdown of trust with their users.

Best practice in fraud prevention is now grounded in advanced AI and biometric technology which deters fraudsters and enables businesses to scale their protection based on risk. It’s what will keep businesses and their users safe in virtual spaces, replicating the level of security and convenience experienced in the physical world, and is why it should earn the title of innovation of the decade.

A digital identity is the online representation of an individual, organization, or entity, encompassing personal information, credentials, and online behavior used for identification and authentication in digital interactions.

Identity fraud occurs when someone uses another person's personal information, such as name or financial details, without their consent to commit fraud or other crimes.

Knowledge-Based Authentication (KBA) is a method of verifying an individual's identity by asking them to answer questions based on their personal history or information that only they should know.

Machine learning in finance refers to the use of algorithms and statistical models to analyze financial data, predict trends, and automate decision-making processes, enhancing efficiency and accuracy.

Biometric technologies are systems that use unique physical characteristics, such as fingerprints or facial recognition, to identify and authenticate individuals, enhancing security in digital transactions.

Explore more articles in the Technology category