DRIVE 4Q13 Results and Index Drivers

The 4Q13 reading rose – What happened to the index components?

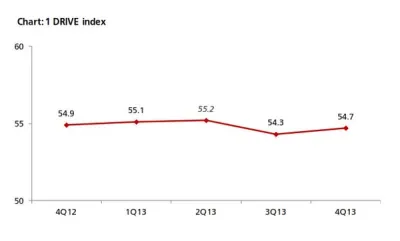

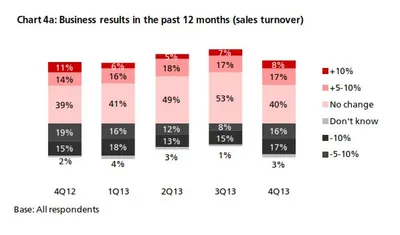

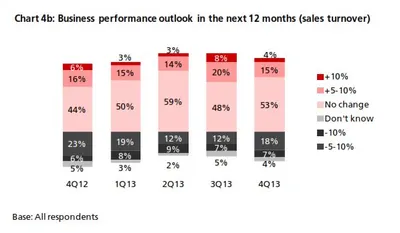

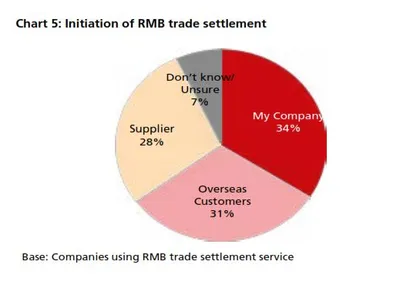

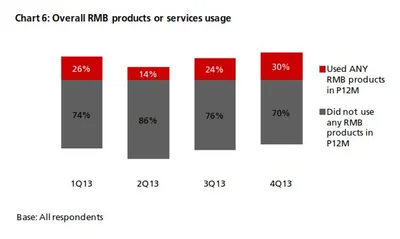

The 4Q13 reading of DRIVE rebounded to 54.7 from 54.3 in 3Q13 (Chart 1). The increase came amid increasing business needs for RMB. In 4Q13, there was a rebound in RMB customer orders and trade settlement, although the proportion of companies using these was below that from a year earlier (Chart 2). In terms of RMB services and products, more companies reported that they are currently using or will consider using RMB payment/receivables and RMB trade services (Chart 3a & 3b) than in all the previous quarters. Interestingly, the general improvement in the usage of RMB services and products in 4Q13 came despite findings showing slightly poorer business performance in the previous 12 months and a more pessimistic business performance outlook for the next 12 months (Charts 4a & 4b). This means that the speed and depth of RMB development in Hong Kong hinges on factors other than local economic and business performance. As Hong Kong is an open economy, its offshore RMB development should be evaluated in the broader context of international RMB development. To put this into perspective, the 4Q13 survey revealed that the initiation of RMB trade settlement is equally split among the Hong Kong companies surveyed (34%), their overseas customers (31%) and their suppliers (28%) (Chart 5). This means that the preferences of overseas players also con- tribute to the RMB development of Hong Kong. Arguably, the preferences of these external parties are shaped in part by their country’s own pace of RMB development. As such, future surveys will continue to monitor Hong Kong’s corporate usage of RMB with a global view in mind.

Finally, regarding access to RMB finance, the perception about the ease of access remained fairly constant in 4Q13 compared to previous quarters.

Key Findings and DBS Expert Analysis

Key findings and DBS insights

* Unless stated otherwise, figures in parentheses represent findings in the previous survey (3Q13)

Rebound in Business Needs for RMB

1. Business needs for RMB have rebounded

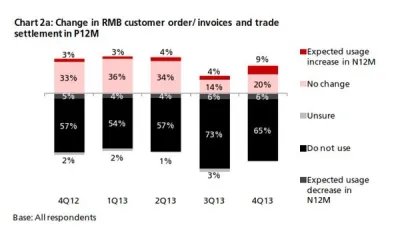

- Business needs for RMB rebounded in 4Q13. Some 35% (24%) of companies surveyed indicated that they had RMB customer orders/invoices in the last 12 months, and 44% (35%) claimed that they would use RMB for these purposes in the next 12 months (Charts 2a & 2b)

- The usage of RMB is already quite common among large corporations (turnover >HK$1 billion). All of the large corporations surveyed indicated that they had RMB customer orders/invoices and trade settlement in the last 12 months

DBS insights

Business needs for RMB is a key indicator of actual RMB acceptance and usage levels at the corporate level. After tracking this component for five quarters, there is no evidence of an uptrend in RMB corporate penetration. In particular, the higher reading in 4Q13 compared to that of 3Q13 should be not be seen as an improvement, as it is merely a recovery from the relatively weak results of 3Q13.

Record Highs in RMB Service Usage

2. Usage of RMB services and products achieved record highs

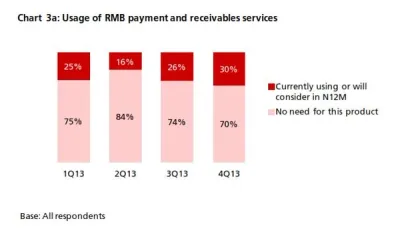

- The number of companies that used any RMB products [1] rose to 30% compared to 24% in 3Q13 (Chart 6). 30% (26%) of companies said they are currently using or will consider using RMB payment and receivables services in the next 12 months. The number of positive responses in 4Q13 is the highest to date (Chart 3a)

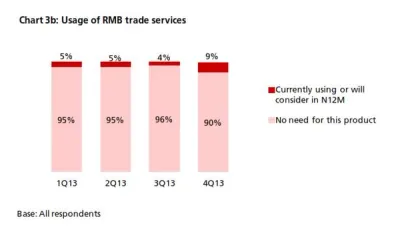

- 9% (4%) of companies said they are currently using or will consider using RMB trade services in the next 12 months. The number of positive responses in 4Q13 is the highest to date (Chart 3b). Of the companies that used trade services (all currencies), 35% (9%) used RMB trade services in the past 12 months. Of those that used trade services (all currencies) but are not currently using RMB trade services, 6% (1%) will consider using them in the next 12 months

DBS insights

The percentage of companies using RMB services and products in 4Q13 was the highest recorded to date. While it is still too early to say that this is the start of an uptrend, the 30% usage rate is quite significant in terms of offshore centre development.

3. Expansion of RMB corporate product scope

- Most companies were only using simple RMB spot conversion for their daily operations. The use of RMB for investment (2%), hedging (4%) or financing (1%) remained negligible

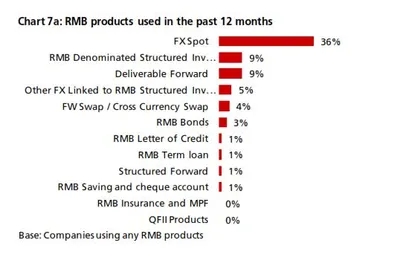

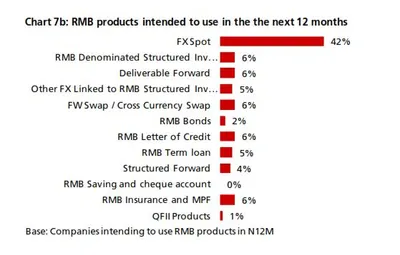

- Of those companies that used any RMB services or products, 36% (57%) used FX spot, but only 9% (10%) had RMB-denominated structured in- vestment deposits and only 1% (5%) had RMB savings and chequing accounts (Charts 7a & 7b).

- However, companies using trade services [2] showed growing interest in RMB investment, finance and hedging products. Some 8% of respondents had RMB investments in 4Q13 (vs. 1% in 3Q); 7% of respondents had RMB financing in 4Q13 (vs. <1% in 3Q), and 12% of respondents were using RMB hedging products in 4Q13 (vs. 3% in 3Q). In 4Q13, more companies showed an intention to use RMB letters of credit (6% intend to use in the next 12 months vs. 1% actual usage in the past 12 months), RMB term loans (5% in N12M vs. 1% in P12M) and RMB structured forwards (4% in N12M vs. 1% in P12M)

- In the RMB financing space, interest is still very limited. Just 1% of companies surveyed said they had been using RMB financing, and only 2% indicated that they are likely to use RMB financing in the next 12 months

DBS insights

The past five quarters of findings showed no consistent trends in the usage of most RMB products. The usage of products such as structured investment deposits (SIDs) and deliverable forwards fluctuated from quarter to quarter.

While efforts to develop RMB products and related financial infrastructure can arouse corporate interest, a sustained take-up of RMB products ultimately de- pends on their business needs for RMB, which showed signs of increasing.

Limited Options for RMB Liquid Assets

4. Usage options for RMB liquid assets are limited

- 35% (44%) of respondents held RMB as part of their liquid assets in the past 12 months

- Most companies are only using simple RMB spot conversions in their daily operations, and not employing RMB funds in more sophisticated ways

- Most companies use the RMB they receive by either paying their suppliers, putting it into bank deposits or converting it to HKD

DBS insights

These findings reflect that companies either did not take advantage of short- term cash management solutions or did not require such solutions. This may also indicate a lack of short-term liquid RMB investment products in the market. As RMB takes up more and more of corporate liquid assets, both financial institutions and companies could begin to explore RMB liquidity management solutions or short-term investments.

Other findings

- RMB usage among Hong Kong companies is still limited, but is slowly increasing

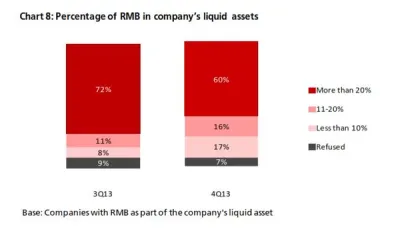

- 33% (19%) of companies [3] reported that RMB assets as a percentage of the company’s liquid assets were more than 10% (Chart 8)

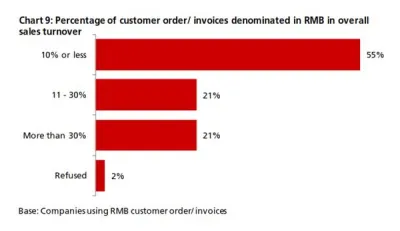

- 42% (34%) of companies [4] reported that RMB customer order/invoices accounted for more than 10% of their overall sales turnover (Chart 9)

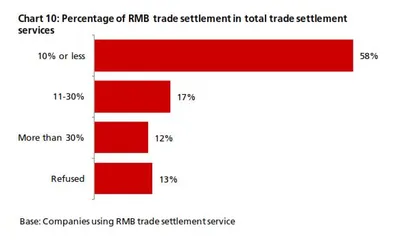

- 29% (24%) of companies [5] reported that RMB trade settlement ac- counted for more than 10% of their total trade settlement services (Chart 10)

Favourable Policy as Main Usage Driver

The outlook: favourable policy support remains the key driver behind corporate usage of RMB

- Despite a slightly more negative outlook for Hong Kong’s general business environment in 4Q13 vs. 3Q13, the corporate usage of RMB saw some improvement in 4Q13

- Five quarters of findings showed no consistent positive correlation be- tween the state of the economy/business outlook and the actual/in- tended corporate usage of RMB

- Since RMB usage is still at an early stage, a positive economic outlook alone – without policy catalysts – is insufficient to further incentivise usage

- The potential relaxation of the personal RMB 20,000 conversion daily cap would be a near-term catalyst for Hong Kong’s offshore RMB market

- This, alongside other policy refinements, would increase Hong Kong’s RMB liquidity pool and lead to more innovation in RMB products

- Personal RMB wealth management products would flourish initially, followed by a gradual pick up in corporate usage

Key Charts & Graphs