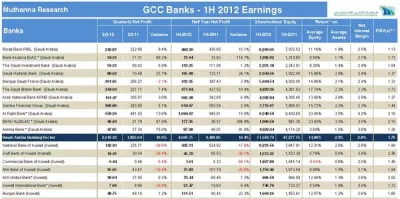

Overview of GCC Banking Sector Results

GCC Banks: Saudi & Qatar Marked Their Dominating-Performance The GCC banks declared their results for 2Q-12 ended June 2012 and in line to industry expectations Saudi Arabia and Qatar – riding high on the economic boom- proved their supremacy in the performance and led overall sector’s growth. Kuwaiti banks extended their provisions for the second quarter consecutively barring few, and thus marked a negative growth on y-o-y basis. In totality, out of 7 markets, 4 markets witnessed a positive growth by their banking while remaining finished off in red.

GCC Banks: Saudi & Qatar Marked Their Dominating-Performance The GCC banks declared their results for 2Q-12 ended June 2012 and in line to industry expectations Saudi Arabia and Qatar – riding high on the economic boom- proved their supremacy in the performance and led overall sector’s growth. Kuwaiti banks extended their provisions for the second quarter consecutively barring few, and thus marked a negative growth on y-o-y basis. In totality, out of 7 markets, 4 markets witnessed a positive growth by their banking while remaining finished off in red.

GCC Banks: Saudi & Qatar Marked Their Dominating-Performance The GCC banks declared their results for 2Q-12 ended June 2012 and in line to industry expectations Saudi Arabia and Qatar – riding high on the economic boom- proved their supremacy in the performance and led overall sector’s growth. Kuwaiti banks extended their provisions for the second quarter consecutively barring few, and thus marked a negative growth on y-o-y basis. In totality, out of 7 markets, 4 markets witnessed a positive growth by their banking while remaining finished off in red.

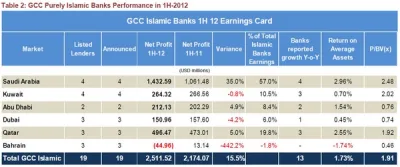

Islamic Banks Increase Profit Share

On the Islamic front, 19 listed entities shared 22.50% of total GCC banking profit, up by 190 basis points, from a year ago, when the Universe was sharing 20.60% of total banking profit. The Islamic Universe performance was purely led by Saudi Arabia, as all of its 4 Islamic lenders reported a growth in their bottom-line, thus reporting a jump of 35% in their total earnings, y-o-y basis. Revealing a similar nature of like composite performance, in the Islamic Universe too, Saudi Arabia shared a shopping 57% share of total Universe earnings.

Key Highlights of Bank Performance

Flash Points on Composite Performance

? Qatar National Bank (QNB), maintained its tag of “the biggest earner”, as the lender marked total net profit of USD 1.14 billion for 1H-2012, immediately followed by the Islamic giant Al Rajhi Bank, which reported a total earning of USD 1.09 billion during the same period. QNB robust performance was purely led by whopping 56% growth in its Loans & Advances y-o-y basis. Its Interest Income jumped by 22% and net interest income (after interest expenses) ballooned by 30% on lower deposit cost.

? On asset base, once again QNB occupied top slot, having total assets of USD 91.13 billion, followed by Emirates NBD with a total asset of USD 81.24 billion. Al-Rajhi stood at 4th position with USD 63.53 billion while Kuwait Finance House (the largest Islamic lender of Kuwait) came at 7th position with total asset of USD 50.15 billion.

Al-Rajhi Leads in Net Interest Income

? On the Net Interest Income (Total Interest/Profit Earned by Loans & Advances minus Interest/Profit Distributed to Depositors), Al-Rajhi outshined all in the GCC and remained the biggest net interest earner of USD 1.24 billion for 1H-2012 followed by QNB with a total net interest earning of USD 1.23 billion. Though Emirates NBD came at 3rd, but in notional term, it earned total interest income of 848 million.

? On the Net Interest Margin (NOM) (Total Net Interest(Profit Earned) /Average Earning Assets for last one year), National Bank of Ras-Al Khaimah earned the highest of NIM at around 9%, thus depicting the best use of earning assets across the sectors. It was followed by National Bank of Umm-Al-Qaiwain with a NIM of 6.91%.

Top Banks by Return on Assets

? Return on Assets: A key performance measuring ratio, as in our opinion, banks’ majority of assets do carry a value which is close to market value. Surprisingly, beating all other major banks, National Bank of Ras-Al-Khaimah (Abu Dhabi) excellent this parameter by giving a best of 5.27% return on total assets, far ahead of United Arab Bank (Abu Dhabi) which earned 3.79%, followed by AL-Rajhi Bank (Saudi Arabia) at 3rd notch with 3.51%. Future Prospects: Most banks are focusing now on recovery efforts and realizing that diversification in the income stream; can only be achieved by expanding beyond the region. Even on capital front, most of major banks are looking forward to conserve their earnings as a proactive measure for future course of debt restructuring or provisions, so as not to depend upon government for any aid, if and so. Finally on the asset quality front, we believe banks may not face any massive deterioration, yet the restructuring pipeline remains a concern. Though, we cannot deny that the sector is reviving from its worst, but we need to understand that this positive-turn is from the lower base, from the time of crisis & provisioning. While overall situation continuous to remain watchful, but valuations of few banks remain attractive considering their historical performance and overall change they aim to redefine their strength in the economic state.

Prepared by:

Shoyeb Ali, Vice President, sali@mic.com.kw

For further enquiries, kindly contact us at:

Muthanna Investment Research

Safat Square, Baitak Tower, 32nd Floor,

Kuwait

mail : irdept@mic.com.kw