Finance

Delinquent Balance Growth: What You Need to Know

Published by Gbaf News

Posted on January 18, 2014

5 min readLast updated: January 22, 2026

Add as preferred source on Google

Published by Gbaf News

Posted on January 18, 2014

5 min readLast updated: January 22, 2026

Add as preferred source on GoogleThe UK is on the gradual road to recovery as it moves steadily out of recession. FICO recently conducted research on UK credit card trends, which demonstrated a reduction in the growth of delinquent balances relative to the growth of current balances, due to cardholders making more timely payments.

The results of the research showed a decrease in the ratio for all delinquent cycles, which suggests an upturn in performance writes Daniel Melo, Senior Director, Fair Isaac Advisors, FICO.

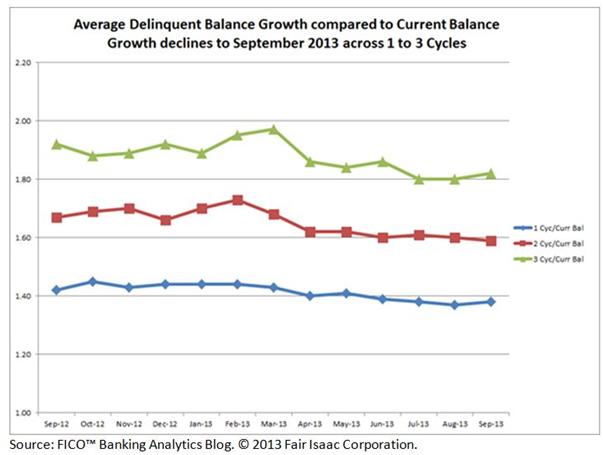

The chart below tracks the growth of 1, 2 and 3 cycle balances to the growth of current balances:

Average X Cycle Balance growth rate (%)

______________________________________

Average Current Balance growth rate (%)

Values over 1 means delinquent balances are growing at a faster rate than current balances.

The results show a decrease in the ratio for all cycles delinquent, suggesting an upturn in the performance. The sample includes over 16 million UK-issued credit cards.

The ratio of 2 Cycle Balance growth to Current Balance growth reached its lowest point over the two-year period in September 2013, with the other ratios at their lowest in August. Year on year, the ratio of 3 Cycle Balance growth to Current Balance growth experienced the largest drop, 5.21%.

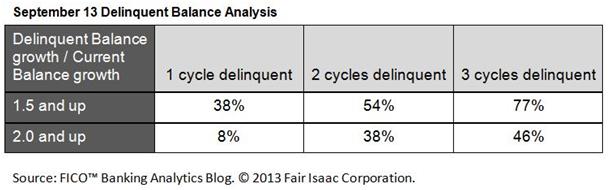

Here’s a bit more information on how these numbers break down:

This data suggests that card issuers should concentrate their collections activities on high-risk, high-balance accounts, while encouraging the growth of current account balances by undertaking pre collections activity.

Daniel Melo

When reviewing accounts at the vintage and delinquency levels, New accounts (<12 months on book) represented the only cohort that showed a growth in the ratio at 2 cycles, but also showed the largest positive change annually for 1 and 3 cycles. Previously, a report from the FICO Benchmark Service expressed concern over increases in New account spending and a decrease in percentage payments to balance, which could indicate future troubles for those accounts. FICO recommends issuers review their treatment of new accounts at 1 cycle, based on balance. Reviewing the performance of accounts against the origination objectives will highlight whether the New account are showing expected results or falling below them, which in turn can help with validating or adjusting originations criteria and cut-off scores.

Industry standard is to treat accounts the same once they mature past the ‘young’ stage, normally 6 months on book, but our data suggests further segmentation and targeted treatment may improve delinquency results.

Veteran accounts (>5 years on book) heavily influence the overall average and have the largest delinquent balances compared to the current balances. This can in part be explained by higher limits, since accounts have had longer to qualify for limit increases. Card issuers may want to consider reviewing performance at the vintage level, in case differing treatment is necessary dependent on the longevity of the account.

The UK is on the gradual road to recovery as it moves steadily out of recession. FICO recently conducted research on UK credit card trends, which demonstrated a reduction in the growth of delinquent balances relative to the growth of current balances, due to cardholders making more timely payments.

The results of the research showed a decrease in the ratio for all delinquent cycles, which suggests an upturn in performance writes Daniel Melo, Senior Director, Fair Isaac Advisors, FICO.

The chart below tracks the growth of 1, 2 and 3 cycle balances to the growth of current balances:

Average X Cycle Balance growth rate (%)

______________________________________

Average Current Balance growth rate (%)

Values over 1 means delinquent balances are growing at a faster rate than current balances.

The results show a decrease in the ratio for all cycles delinquent, suggesting an upturn in the performance. The sample includes over 16 million UK-issued credit cards.

The ratio of 2 Cycle Balance growth to Current Balance growth reached its lowest point over the two-year period in September 2013, with the other ratios at their lowest in August. Year on year, the ratio of 3 Cycle Balance growth to Current Balance growth experienced the largest drop, 5.21%.

Here’s a bit more information on how these numbers break down:

This data suggests that card issuers should concentrate their collections activities on high-risk, high-balance accounts, while encouraging the growth of current account balances by undertaking pre collections activity.

Daniel Melo

When reviewing accounts at the vintage and delinquency levels, New accounts (<12 months on book) represented the only cohort that showed a growth in the ratio at 2 cycles, but also showed the largest positive change annually for 1 and 3 cycles. Previously, a report from the FICO Benchmark Service expressed concern over increases in New account spending and a decrease in percentage payments to balance, which could indicate future troubles for those accounts. FICO recommends issuers review their treatment of new accounts at 1 cycle, based on balance. Reviewing the performance of accounts against the origination objectives will highlight whether the New account are showing expected results or falling below them, which in turn can help with validating or adjusting originations criteria and cut-off scores.

Industry standard is to treat accounts the same once they mature past the ‘young’ stage, normally 6 months on book, but our data suggests further segmentation and targeted treatment may improve delinquency results.

Veteran accounts (>5 years on book) heavily influence the overall average and have the largest delinquent balances compared to the current balances. This can in part be explained by higher limits, since accounts have had longer to qualify for limit increases. Card issuers may want to consider reviewing performance at the vintage level, in case differing treatment is necessary dependent on the longevity of the account.

Explore more articles in the Finance category