INTRODUCTION

This is a summary of the first-ever survey of the Israeli hedge fund industry. The survey seeks to introduce the industry to the global market as well as highlight its emergence and growth in recent years.

Growth and Development of Israeli Hedge Funds

Israel, already acknowledged as a global center for innovation in high-tech, is now making major strides in the financial services industry. Over the past decade, deregulation and new legislation in securities and tax law, together with structural changes in the institutional market, have made it possible for a robust finance industry to emerge. Israeli financial institutions have evolved into sophisticated global investors, deploying tens of billions of dollars in investments outside of Israel. Israel’s impressive academic and scientific infrastructure, continuing immigration of professionals from western countries and a developed economy with a strong entrepreneurial culture are all fueling the rapid growth of the finance industry. It was these same elements which helped create the high-tech industry in the early nineties.

Although in its earliest stages, it is Tzur’s belief that the Israeli hedge fund industry will grow to become a recognized center of hedge fund activity during the coming decade. As is evident from the survey findings, there is still much to accomplish before this goal can be achieved. It is Tzur’s hope that this survey will serve as just one milestone in the long road ahead, influencing favorable government policy toward the hedge fund industry and generating interest within the international investment community.

For the complete survey or any inquiries, please contact info@tzurmanagement.com.

ABOUT TZUR MANAGEMENT

Tzur Management (“Tzur”) serves as a platform for the Israeli fund industry, offering Israeli managers a wide array of services ranging from back-office and fund administration to hosting and capital introduction. Tzur is an affiliate of Columbus Avenue LLC, a $6 billion fund administrator based in New York. For more information on Tzur and its services, please contact info@tzurmanagement.com.

INDUSTRY OVERVIEW

Over the past five years, the Israeli hedge fund industry has grown considerably. Only a decade ago, Israel had little in the way of a hedge fund industry. Regulation had stifled the emergence of an investment industry and limited investment professionals’ activities in global markets.

However, structural changes in the institutional markets in the early 2000s that allowed broader allocation of investments, coupled with deregulation and new legislation in securities and tax law enabled the early growth of a modern finance industry. As a result, we are now witnessing an industry on the verge of a sustained period of rapid development.

Increase in Number of Fund Managers

Number of fund managers in Israel

Out of 34 fund managers participating in the survey only 13 were operational prior to 2006. There has been a 162% increase in the number of funds in Israel since 2006.

Tzur believes that this growth rate is indicative of the Israeli hedge fund market as a whole and estimates that the number of funds in Israel has grown to above 60 in recent years. Considering that this figure does not include numerous proprietary traders scattered throughout the country as well as many aspiring managers planning launches of new funds, the message is of a budding investment industry with as many as 100 active fund managers.

Expansion of Assets Under Management

Assets under management

The growth of the Israeli hedge fund industry is also apparent in the industry’s assets under management (AUM).

The creation of new funds has brought fresh assets into the industry, while older, more established funds are increasingly attracting investment from institutions and private individuals. These factors have contributed to the growth in assets under management of the 34 participating fund managers in our survey to $1.57 billion as of March 31, 2012.

Tzur conservatively estimate that total assets under management of roughly 60 Israeli hedge funds have grown in recent years to just under $2 billion.

Asset concentration

Concentration of assets under management in the Israeli hedge fund industry is similar to the global investment industry in that the largest funds manage the majority of the assets. As of March 31, 2012, 75% of assets under management were held by 20% of the industry’s fund managers.

The growth of the industry can be characterized by the following attributes:

- Small launches: Despite the large number of fund launches since 2008, no fund launched with more than $15 million and growth of these small funds has been modest.

- Newer funds take longer to grow asset base: Less than 20% of the total assets under management are managed by funds created from 2008 to the present.

- Asset ramp, persistent and methodical: Ramping up the assets of a fund has taken considerably longer in Israel. The number of funds managing in excess of $50 million has only grown from five to eight since 2009.

Asset growth

Clearly, limited access to capital has hindered the industry’s growth. Tzur believes that this stems from limited knowledge of the Israeli hedge fund market among investors. While this has been a cause for concern among Israeli managers, we expect awareness of local managers to grow over the coming years leading to significant AUM growth.

The Israeli hedge fund industry is already growing as demonstrated by the growth in AUM. Among funds reporting historical data, AUM grew 30% in 2011, and an additional 10% through March 2012.

Challenges With Foreign Investment

Foreign investors

A key obstacle for many investment managers is getting the attention of investors. This is particularly true with regard to marketing to foreign investors. International investors are generally unaware of the nascent Israeli hedge fund industry and many of those who are aware of its existence still consider it too small to devote resources.

Additionally, despite a tax regime favorable to foreign investors (investors don’t pay local taxes on investment with Israeli fund managers), concerns surrounding Israeli tax laws have been a hurdle for many first-time foreign investors.

As part of the survey, managers were asked for their opinion regarding foreign investment in Israeli hedge funds. Over 80% of participants agreed that foreign investors are not aware of the Israeli hedge fund industry, resulting in a lack of investment.

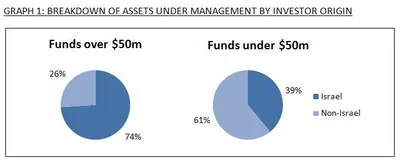

Assets under management by investor origin

Turning to the data itself, it is clear that the local industry is still currently supported by local investors. More than two-thirds of total assets under management come from Israeli investors, with less than a third raised from international sources.

However, graph 1 below reveals a surprising distinction between the larger and smaller funds. While the larger funds have received most of their funding from local Israeli sources, the smaller funds have been more successful in recruiting investors from overseas. Analysis of the data confirms that this is not a case of a few investments from overseas skewing the results of smaller funds, but rather a trend among smaller and in most cases newer funds succeeding in securing foreign investors.

Diversity of Investment Strategies

INVESTMENT STRATEGIES

As the hedge fund industry grows in size, it becomes increasingly diverse and sophisticated. Although it is still in its early stages, the Israeli hedge fund industry includes funds investing in a diverse set of strategies, asset classes and geographies.

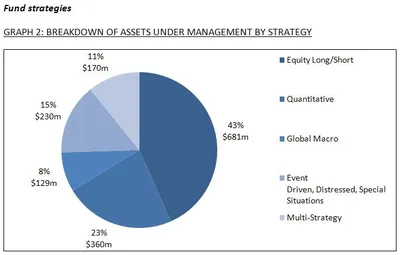

Equity Long/Short funds currently hold the largest share of the industry with 43% of assets under management, and quantitative strategies are next in line with 23%.

Tzur’s research into recent fund launches, however, demonstrates that the trend is towards a wider distribution among the various strategies. New funds have launched across all five strategies with the biggest increase among quantitative strategies.

The number of quant strategies operating has more than doubled since 2008, and many of the proprietary trading operations and planned new fund launches are quantitative in nature as well.

Tzur believes that quantitative strategies play to Israel’s strengths, leveraging the mathematical and statistical brainpower that has been the catalyst behind the massive growth of several of Israel’s industries, notably telecommunications, software and medical devices.

Geographic Diversification Beyond Israel

Geographic allocation

Although the perception among many may be that Israeli funds are focused primarily on local markets, in fact, Israeli funds are quite diversified geographically. Half of the funds participating in the survey have no direct exposure whatsoever to the markets in Israel.

Overall, about half of assets under management are invested outside of Israel, and this ratio applies fairly evenly across all strategy types. Diversification outside of Israel is increasing rapidly, as only 2 of the 13 funds created since 2009 allocate capital to the local market.

PERSONNEL

Portfolio managers

Of the 40 participating portfolio managers:

- Born overseas: a third of Israeli portfolio managers were born abroad, and immigrated to Israel from the United States, Europe or South Africa.

- Leading academic institutions: nearly half of all portfolio managers studied abroad at top universities in the United States or Europe, with a quarter of portfolio managers having attended Ivy League schools.

- Multiple degrees: furthermore, two-thirds of all portfolio managers have attained a second degree or doctorate in their respective fields.

Personnel

The 30 funds who participated in this section employ over 160 individuals ranging from front office positions (portfolio managers, traders, risk managers, research analysts) to back office and administrative functions.

Tzur estimate that the hedge fund industry as a whole employs close to 300 people.

APPENDIX: NOTES ON PERFORMANCE

This survey was conducted with the intention of providing an overview of the Israeli fund market without a specific focus on performance. However, twenty Israeli hedge funds agreed to share their performance data which we present here as compared to the HFRX Global Hedge Fund Index.