REL Consultancy standardizes collection and introduces dynamic credit risk processes to produce significant and sustainable gains in accounts receivable performance for Lennox International – while revenues continue to grow

Lennox International Inc. is a leading provider of climate control solutions for heating, air conditioning and refrigeration markets around the world. It had annual sales of nearly $3.0 billion (€2.3 billion) in 2012.

Identifying Opportunities for Cash Flow Improvement

Opportunities to standardize, simplify, automate

Lennox initiated a program to focus on accounts receivable performance companywide to support cash flow and other goals. Peter Jackson and Joe Reitmeier, Lennox vice presidents of finance for financial shared services, asked for an independent assessment of current collections and credit processes and to identify opportunities for improvement. The initial review determined that by standardizing, simplifying and automating key collections and credit processes, Lennox could achieve significant improvements in accounts receivable performance.

Based on the review, the two Lennox executives and REL met with senior leadership and mapped out a project plan for delivering rapid impact.

Customer Segmentation and Collection Standardization

Segmentation and standardization as the foundation for improving collections

Jackson hired Randy Dacus, Lennox’s director of customer financial services, after the project began to implement and build upon the best practices introduced by REL. “Before you can tackle anything, you need to understand what you’re tackling,” said Dacus. “REL helped us do just that. They started by developing a comprehensive picture of our customer base and segmenting it into different categories based on payment performance.”

This segmentation analysis enabled Lennox to create standardized, proactive collection strategies for each customer segment and protocols for applying those strategies consistently across the business. For example, all customers fitting a certain payment profile now receive a call before an invoice is due and then a letter seven days after the due date. Escalation processes may also involve the sales function in collections for certain situations, for example, when a particular amount threshold is reached. For higher values, the vice president of sales or business unit chief financial officer may become involved.

“Standardization in collections strategy and approach has translated into more predictable collections,” said Dacus. “You want predictability in collections and cash flow – for reinvestment purposes, to pay down debt, and to put the business in a better position to grow and increase shareholder value.”

Implementing Dynamic Credit Risk Management

Dynamic credit risk management processes

Dynamic credit risk management processes

On the credit side, a cornerstone of the work was replacing decentralized approaches for extending credit and a static approach to reviewing existing credit terms with a standardized, dynamic approach applicable to all new and existing customers.

Most companies review individual customers’ credit only once per year or so; however, with these long intervals, companies could overlook risk opportunities as conditions change. REL helped Lennox create a dynamic credit review process under which every customer gets a credit grade each month based on past sales behavior and payment performance. The model pulls data from internal and external (credit agency) sources and then weights the data based on a prioritized set of factors. REL used algorithms developed with Lennox and customized for the business. The result is a consistent approach to setting credit terms and the ability to identify specific cases – positive and negative – from among its thousands of customers for manual review and/or adjustment.

Lennox has continued to build on this model by automating the related processes. “REL created a sound framework – the building. We’ve added the drywall, cement, carpet and other accoutrements over time,” Dacus noted. “This approach has enabled us to increase attention to areas that require focus and spend less time managing customers that pay predictably.”

Fostering Collaboration Between Sales and Credit

Credit and sales support – and collaboration

Gaining the support of both the sales and credit functions was essential, as was developing strong collaboration between them.

“One of REL’s biggest contributions was to help us demystify credit and collection best practices for the sales management function through effective, straightforward communications,” said Jackson. “Before finalizing its proposed recommendations, REL listened to our sales function and to our customers. None of its recommendations were created in a vacuum; they were developed to meet the needs of our internal and external customers. Ultimately, REL helped us quantify how these new practices would be accretive to our return on invested capital – and then demonstrate that growing sales and improving cash flow are not mutually exclusive concepts.”

“We have a very tenured credit organization with a lot of institutional knowledge about our customers,” added Dacus. “We wanted to embrace and retain that element, while still making needed changes. There were some who felt that introducing rigor and standardization would take away from their flexibility to serve customers and would impair revenues. What it really did was exactly the opposite.”

Collectors found that when they followed the prescribed rigor, their numbers improved and they were rewarded accordingly. Dacus said morale improved along with accounts receivable performance.

Lennox also engaged the sales function in developing and executing new processes. “We explained the changes to the sales function in a different way than we did to the finance function,” Dacus said. “Having a clear picture of our portfolio composition enabled us to articulate complex issues in a simple but meaningful way.”

He says coordination between the sales and credit organizations has “never been better. We have people with more than 40 years at Lennox who cannot recall a time when sales and credit had a more cohesive approach to the marketplace.”

Strengthening Leadership and Accountability

Enhancing leadership and accountability

As part of the project, REL also evaluated Lennox’s credit organization structure and assessed capabilities for implementing and advancing the new processes. This led to the addition of a separate function to provide general credit and portfolio risk oversight and also to focus on the small percentage of new credit applications not auto-approved using proprietary commercial scoring models.

Change management played a key role in process improvement. To make sure enhancements were implemented effectively, Lennox devoted more time to training, coaching and counseling activities. In addition, REL helped Lennox introduce a comprehensive set of metrics based on management goals and deployed them from the division level down to individual credit personnel. “Our leadership expected significant improvement, so we needed to do a better job of holding people at all levels in our organization accountable,” said Dacus.

Driving Consistency Through Automation

Automation essential to consistency and improvement

Dacus said Lennox continues to look for ways to automate the processes REL helped put in place. For example, Lennox now has automated credit limit scoring. The company also introduced paperless processing and storage for credit applications, as well as a workflow tool that notifies sales managers when a credit application is approved. This workflow enhancement prompts the sales organization to follow up on the approval by notifying the customer and proactively asking for an order. In all, the changes have reduced the credit approval process from two weeks to one day.

Introducing change to customers

Because the new processes required contacting many customers earlier in the collection cycle, it was important to explain why. Lennox provided its credit and sales teams with scripts for communicating the changes in a positive and consistent manner. This dialogue not only helped ease concerns, it enabled collectors to identify cash flow issues early on and look for ways to assist.

“Lennox, as a whole, has a big push around listening to customers,” said Dacus. “Our sales organization does a good job of vetting who we choose as our customers and vendors, and we want to do what we can to keep customers and keep them viable. Through the processes we’ve put in place, we are listening more closely and addressing issues proactively because we are touching them earlier in the process, before the situation becomes untenable or difficult to unwind.”

Excellent Results

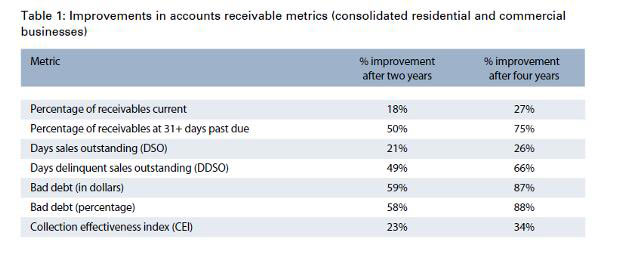

The efforts produced improvements quickly and in all key areas measured. After completing introduction of the new collections and credit processes, Lennox measured significant two-year improvements. Another two years later, the improvements continue. “We are extremely happy with the results of this effort, both short and long term. We’re continuing to see significant year-over-year improvements, even several years after the project phase ended.” said Dacus (Table 1).

Notably, the changes have also had a positive impact on customer relations, which ultimately affects revenue. For example, dynamic credit risk grading has enabled Lennox to reduce significantly the number of order holds in place for low-risk customers. Conversely, improved visibility of payment issues and increased dialogue with higher-risk customers has enabled Lennox to work with and help keep valued customers viable. “I’ve received handwritten thank you notes from customers we’ve assisted through difficult situations using this process,” said Dacus. “That’s just as rewarding as the quantitative results.”

REL Consultancy standardizes collection and introduces dynamic credit risk processes to produce significant and sustainable gains in accounts receivable performance for Lennox International – while revenues continue to grow

Lennox International Inc. is a leading provider of climate control solutions for heating, air conditioning and refrigeration markets around the world. It had annual sales of nearly $3.0 billion (€2.3 billion) in 2012.

Opportunities to standardize, simplify, automate

Lennox initiated a program to focus on accounts receivable performance companywide to support cash flow and other goals. Peter Jackson and Joe Reitmeier, Lennox vice presidents of finance for financial shared services, asked for an independent assessment of current collections and credit processes and to identify opportunities for improvement. The initial review determined that by standardizing, simplifying and automating key collections and credit processes, Lennox could achieve significant improvements in accounts receivable performance.

Based on the review, the two Lennox executives and REL met with senior leadership and mapped out a project plan for delivering rapid impact.

Segmentation and standardization as the foundation for improving collections

Jackson hired Randy Dacus, Lennox’s director of customer financial services, after the project began to implement and build upon the best practices introduced by REL. “Before you can tackle anything, you need to understand what you’re tackling,” said Dacus. “REL helped us do just that. They started by developing a comprehensive picture of our customer base and segmenting it into different categories based on payment performance.”

This segmentation analysis enabled Lennox to create standardized, proactive collection strategies for each customer segment and protocols for applying those strategies consistently across the business. For example, all customers fitting a certain payment profile now receive a call before an invoice is due and then a letter seven days after the due date. Escalation processes may also involve the sales function in collections for certain situations, for example, when a particular amount threshold is reached. For higher values, the vice president of sales or business unit chief financial officer may become involved.

“Standardization in collections strategy and approach has translated into more predictable collections,” said Dacus. “You want predictability in collections and cash flow – for reinvestment purposes, to pay down debt, and to put the business in a better position to grow and increase shareholder value.”

Dynamic credit risk management processes

Dynamic credit risk management processes

On the credit side, a cornerstone of the work was replacing decentralized approaches for extending credit and a static approach to reviewing existing credit terms with a standardized, dynamic approach applicable to all new and existing customers.

Most companies review individual customers’ credit only once per year or so; however, with these long intervals, companies could overlook risk opportunities as conditions change. REL helped Lennox create a dynamic credit review process under which every customer gets a credit grade each month based on past sales behavior and payment performance. The model pulls data from internal and external (credit agency) sources and then weights the data based on a prioritized set of factors. REL used algorithms developed with Lennox and customized for the business. The result is a consistent approach to setting credit terms and the ability to identify specific cases – positive and negative – from among its thousands of customers for manual review and/or adjustment.

Lennox has continued to build on this model by automating the related processes. “REL created a sound framework – the building. We’ve added the drywall, cement, carpet and other accoutrements over time,” Dacus noted. “This approach has enabled us to increase attention to areas that require focus and spend less time managing customers that pay predictably.”

Credit and sales support – and collaboration

Gaining the support of both the sales and credit functions was essential, as was developing strong collaboration between them.

“One of REL’s biggest contributions was to help us demystify credit and collection best practices for the sales management function through effective, straightforward communications,” said Jackson. “Before finalizing its proposed recommendations, REL listened to our sales function and to our customers. None of its recommendations were created in a vacuum; they were developed to meet the needs of our internal and external customers. Ultimately, REL helped us quantify how these new practices would be accretive to our return on invested capital – and then demonstrate that growing sales and improving cash flow are not mutually exclusive concepts.”

“We have a very tenured credit organization with a lot of institutional knowledge about our customers,” added Dacus. “We wanted to embrace and retain that element, while still making needed changes. There were some who felt that introducing rigor and standardization would take away from their flexibility to serve customers and would impair revenues. What it really did was exactly the opposite.”

Collectors found that when they followed the prescribed rigor, their numbers improved and they were rewarded accordingly. Dacus said morale improved along with accounts receivable performance.

Lennox also engaged the sales function in developing and executing new processes. “We explained the changes to the sales function in a different way than we did to the finance function,” Dacus said. “Having a clear picture of our portfolio composition enabled us to articulate complex issues in a simple but meaningful way.”

He says coordination between the sales and credit organizations has “never been better. We have people with more than 40 years at Lennox who cannot recall a time when sales and credit had a more cohesive approach to the marketplace.”

Enhancing leadership and accountability

As part of the project, REL also evaluated Lennox’s credit organization structure and assessed capabilities for implementing and advancing the new processes. This led to the addition of a separate function to provide general credit and portfolio risk oversight and also to focus on the small percentage of new credit applications not auto-approved using proprietary commercial scoring models.

Change management played a key role in process improvement. To make sure enhancements were implemented effectively, Lennox devoted more time to training, coaching and counseling activities. In addition, REL helped Lennox introduce a comprehensive set of metrics based on management goals and deployed them from the division level down to individual credit personnel. “Our leadership expected significant improvement, so we needed to do a better job of holding people at all levels in our organization accountable,” said Dacus.

Automation essential to consistency and improvement

Dacus said Lennox continues to look for ways to automate the processes REL helped put in place. For example, Lennox now has automated credit limit scoring. The company also introduced paperless processing and storage for credit applications, as well as a workflow tool that notifies sales managers when a credit application is approved. This workflow enhancement prompts the sales organization to follow up on the approval by notifying the customer and proactively asking for an order. In all, the changes have reduced the credit approval process from two weeks to one day.

Introducing change to customers

Because the new processes required contacting many customers earlier in the collection cycle, it was important to explain why. Lennox provided its credit and sales teams with scripts for communicating the changes in a positive and consistent manner. This dialogue not only helped ease concerns, it enabled collectors to identify cash flow issues early on and look for ways to assist.

“Lennox, as a whole, has a big push around listening to customers,” said Dacus. “Our sales organization does a good job of vetting who we choose as our customers and vendors, and we want to do what we can to keep customers and keep them viable. Through the processes we’ve put in place, we are listening more closely and addressing issues proactively because we are touching them earlier in the process, before the situation becomes untenable or difficult to unwind.”

Excellent Results

The efforts produced improvements quickly and in all key areas measured. After completing introduction of the new collections and credit processes, Lennox measured significant two-year improvements. Another two years later, the improvements continue. “We are extremely happy with the results of this effort, both short and long term. We’re continuing to see significant year-over-year improvements, even several years after the project phase ended.” said Dacus (Table 1).

Notably, the changes have also had a positive impact on customer relations, which ultimately affects revenue. For example, dynamic credit risk grading has enabled Lennox to reduce significantly the number of order holds in place for low-risk customers. Conversely, improved visibility of payment issues and increased dialogue with higher-risk customers has enabled Lennox to work with and help keep valued customers viable. “I’ve received handwritten thank you notes from customers we’ve assisted through difficult situations using this process,” said Dacus. “That’s just as rewarding as the quantitative results.”