John Dowdall, Global Business Development

Solvency II Overview and Regulatory Impact

Background

The introduction of the Solvency II regulation brings to an unprecedented level the data requirements that asset managers already face from a myriad of regulations and legislation.

The Directive seeks to harmonise the capital adequacy requirements for insurance firms operating in the European Union. While it is of European origin, Solvency II has wide-ranging implications and ramifications that reverberate deeply into the global asset management community.

This tsunami of regulation has proven one thing: the old order model no longer fits. In the past sourcing fund data involved throwing bodies at the problem and creating a swathe of manual and semi-automated processes built around a veritable cottage industry of Excel macros and Access databases. Now though, the level of data being required and the sensitivity of that data, in combination with incredibly tight turnarounds means that the old order thinking no longer fits.

Changing Role of Asset Managers

Faced with Solvency II, one of the greatest regulatory shakeups in the history of European financial oversight, the insurance business is turning to its asset management service providers for help. The regulation is asking end investors to develop ‘look-through’ transparency over their investments, in order to deliver an accurate assessment of the capital required to mitigate against risks.

Insurers are already spending hundreds of millions of pounds complying with Solvency II. Developing a system that enables them to look-through fund-of-fund data to identify the ultimate asset will require unprecedented levels of data standardisation, data licensing alterations and data transfer processes.

Transparency Challenges and Data Disclosure

Beyond the technical challenges and the costs, asset managers are being asked to disclose their holdings data, which can ultimately reveal the investment strategy they are employing. This in turn exposes the fund to front-running and strategy-free-riding, neither of which is in the interest of the existing investors or indeed of the fund manager.

While Solvency II is designed to ensure that insurance companies understand the risk within both the asset and liability sides of their balance sheet with a view to defining the correct amount of capital that should be set aside to mitigate these risks and avoid systemic risk in the industry, it may well cause systemic risk in certain areas of capital markets and funds.

From an asset manager’s perspective, this regulation is not something that they are required to comply with. However, the onus is being put on them to enable their largest investor to comply. This requires them to provide their holdings data in a timely manner to insurance investors. Providing this in a delayed manner 15 or 30 days after month end will not suffice, so their IPR & investment strategy is being looked for between day 1 and 3 at the start of the month.

Should they not be able to do this, the investment made by the insurer is considered by the regulation as non-transparent or a ‘black box’ investment. This would require the insurer to set aside 49% in capital to retain the investment, or divest and seek a more transparent product. The risk to asset managers’ assets under management is considerable.

Consequences of Insufficient Transparency

To provide some scope of what is at risk, one only has to look at the size of the European insurance investment portfolio, €7.5 trillion (2010). The scale of this investment, and the possibility that insurers will change their investment strategy and move away from investment products like funds, should they not be willing or able to provide the required transparency, is significant.

Research carried out earlier this year by Blackrock and the Economist Intelligence Unit where they surveyed 233 European insurance organisations, who themselves represent more than half of the total European insurance investment portfolio (approx. €3.75 trillion), stated that 92% of respondents felt that the inability to gain access to look-through would hamper their ability to invest in certain products.

It should be noted that it is not only asset managers that will be affected by this, as any loss in AUM for them also will affect third party administrators’ and service providers’ assets under administration as well as anyone who earns basis points fees in the funds industry. The question is: what are all these organisations doing to address this issue and protect their business?

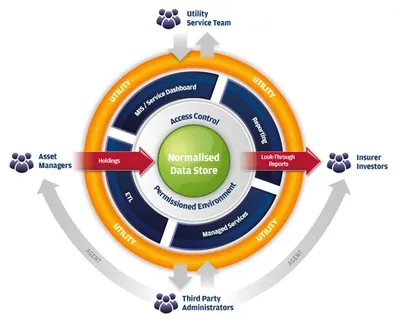

MoneyMate’s Solution for Look-Through

MoneyMate has a solution.

Asset managers and their administrators need some method to be able to protect AUM & AUA, while protecting investment strategy and retaining control of their data. A utility that provides asset managers with the ability to permission which firms gets their data and retain control is required.

MoneyMate has launched a Solvency II “Look-Through and Reporting Utility” which establishes data connectivity between asset managers and insurers to facilitate an effective response to the stringent reporting demands of Solvency II. The look-through and reporting utility will enable buy-side participants to provide holdings data to insurance investors in a permissioned and controlled environment.

It is also important that asset managers get something in return. Today, asset managers have only a partial view of who their investors are. They can understand to some extent what exposure they have to insurance investors who invest as a direct investor, but have little or no transparency of insurers who invest indirectly via other funds, products or through platforms. A utility that provides asset managers with the identification of their ultimate investor will allow them to make strategic decisions. If able to identify which insurers have invested in their funds that would have a high capital requirement, say 30%, they can now engage those investors and introduce them to other funds they have designed to be Solvency II friendly with a lower capital requirement (5-10%) which have a similar risk-adjusted IRR. This ability allows asset managers retain their existing mandates and provides insurers with a level of service not currently available.

Benefits for Fund Managers and Administrators

Benefits the fund industry will receive due to this collaboration:

- Utility will enable asset managers to protect investment strategies while ensuring that their funds are Solvency II friendly

- Utility provides data connectivity between asset managers, third party administrators and insurers to facilitate an effective response to the stringent reporting demands of Solvency II

- Enables insurers and their service providers to gain access to transparent, granular data from a single source and in a standardised format

- A single repository, accessible for hundreds of asset managers, providing look-through even across complex investment structures including fund-of-funds.