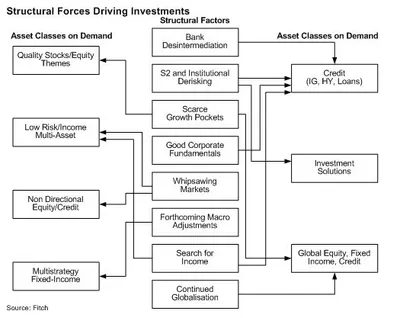

European institutional investors are now de-risking, while seeking out yield to meet commercial or actuarial targets. Credit is particularly appealing to institutional investors, while insurers favour investment grade corporates and pension funds target high yield and emerging markets, at the expense of equity. Sub-asset classes, such as inflation linkers, tactical asset allocation funds, infrastructure or cash are benefiting from some institutional interest, notably from Dutch and UK pension funds and continental European insurers. Managers that are not well positioned on credit – notably specialties (high yield, short term, emerging markets) are likely to lose institutional market share.

Optimizing Investment Strategy Focus Areas

Focusing the portfolio of expertise

To be successful, investment strategies where demand is anticipated and where the manager is credible, will require strengthened resources (front office, commercial, product specialists, staff with international profiles); increased critical mass (by merging funds, using master feeders, moving client money); heightened commercial efforts (referencing, distribution, communication, ratings); and adoption of international standards (funds’ benchmark, product name and domicile).

Restructuring Underperforming Offerings

Conversely, investment strategies where demand is expected to be weak and/or the manager lacks credibility will need to be scaled down, either by closing funds, outsourcing management or by using funds of funds or funds of mandates.

Selective Expansion Into New Activities

Expanding selectively

In order to remain competitive, asset managers in our view should not hesitate to expand into “neighbouring” activities, despite the resource and process adjustment this requires. For example, a high yield manager may consider expanding into loans, or a loan manager into high yield, as the issuer pool is similar.

Likewise, moving into the diversified income space is a logical progression for a European equity manager, given the overlap between large-cap stocks and investment-grade credit issuers. Such a development would require the recruitment of bond portfolio managers and the set-up of a top down allocation process. Long only stock and bond pickers are also well placed to navigate sideways markets by developing absolute return offerings.

Capitalizing on Structural Industry Trends

# on long-term trends

Bank deleveraging and globalisation should also benefit the European asset management industry. The European banks’ deleveraging process is expected to generate market financing needs representing roughly 10% to 20% of the current European investor asset base (pension funds, insurance companies, mutual funds), New areas of growth fuelled by these factors include: global equity or bond products; emerging markets; senior secured high yield; direct lending; and real assets. Many of these are new to asset managers, who must develop scale and credibility if they wish to successfully compete in these areas. Yet in most cases, doing so demands serious investment in terms of local analysts, sourcing channels, and technical and legal knowledge. Fitch believes that acquisition and team lift out are the only viable options.

Investment Needs for New Capabilities

However, developing new activities, for example in global equity or senior secured high yield, requires significant investments in terms of personnel and/or acquisitions. Managers unwilling or unable to commit in these areas now may find themselves less able to compete in the near future.