Investing

Czech Republic Marks Half Year Since Start of Pension Reform

Published by Gbaf News

Posted on September 11, 2013

6 min readLast updated: January 22, 2026

Add as preferred source on Google

Published by Gbaf News

Posted on September 11, 2013

6 min readLast updated: January 22, 2026

Add as preferred source on Google

What has changed in the Czech Republic half a year after the introduction of pension reform? People no longer rely on state pensions and nearly 90% of Czechs under 35 years of age plan to save for their retirement. This is confirmed by research from the agency Millward Brown for the Czech daily Deník.

CZECH REPUBLIC PENSION REFORM

Approximately 78% of people believe that the state will not be able to maintain paying the current pension amounts in the future. About 71% of respondents said they would find a way to save an amount for their retirement. About 89% of respondents under 35 years of age said they either have been saving or are going to save for their retirement.

However, the survey also revealed that more than half of the Czech working population still do not have enough information about saving options. Nearly three fifths of respondents said they don´t understand the three pillar system of the current pension system. They regard the biggest problem to be the newly introduced second pillar of retirement savings. A system under which of the 28% deduction for social security a person saving for retirement can direct 3% to a personal retirement account at a selected financial institution if they contribute 2% of their gross wages from their own resources. When asked whether they know what percentage they would have to save from their deductions only a fifth of respondents answered correctly.

The question regarding what people are most concerned about in relation to saving for retirement also revealed that the respondents do not really understand pension reform. Most are concerned that the retirement company will go bankrupt or that they will be defrauded of their money. One of the main changes that pension reform has introduced is separation of the property of participants in saving from company property. It is also interesting that people trust companies managing the third pillar of the pension system, but their trust in the second pillar is minimal. They do not realise that in both cases the same management company is involved.

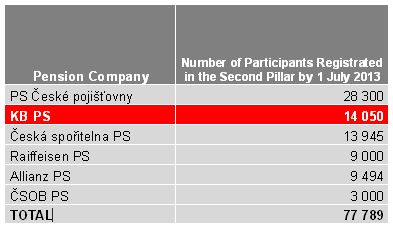

According to the survey participation in the second pillar is being considered by around 9% of people of active age. In absolute expression this represents about 650,000 people. Now that the sales results for the first half of the year are known and the second pillar has also been opened for people over the age of 35 there are really only just over 77,000 participants in it.

Where is the mistake? The entire reform has been negatively affected by a strong campaign waged against it by the most powerful opposition party. Ever since pension reform began the opposition has stated repeatedly that its post-election priority (following the collapse of former Prime Minister Petr Nečas’ government and early elections called for the Czech Republic in October) will be cancellation of the second pillar of pension reform. Participants in it will reportedly be able to withdraw their savings or transfer them to the third pillar. The expected winner of the elections the Czech Social Democratic Party intends to support it in the future. It plans for example to do more to motivate companies to contribute to their employees’ savings. Whether or not the new government will find a recipe for a satisfactory solution for the ageing population and the dramatic worsening demographics of the Czech Republic’s population in the forthcoming period remains to be seen.

What has changed in the Czech Republic half a year after the introduction of pension reform? People no longer rely on state pensions and nearly 90% of Czechs under 35 years of age plan to save for their retirement. This is confirmed by research from the agency Millward Brown for the Czech daily Deník.

CZECH REPUBLIC PENSION REFORM

Approximately 78% of people believe that the state will not be able to maintain paying the current pension amounts in the future. About 71% of respondents said they would find a way to save an amount for their retirement. About 89% of respondents under 35 years of age said they either have been saving or are going to save for their retirement.

However, the survey also revealed that more than half of the Czech working population still do not have enough information about saving options. Nearly three fifths of respondents said they don´t understand the three pillar system of the current pension system. They regard the biggest problem to be the newly introduced second pillar of retirement savings. A system under which of the 28% deduction for social security a person saving for retirement can direct 3% to a personal retirement account at a selected financial institution if they contribute 2% of their gross wages from their own resources. When asked whether they know what percentage they would have to save from their deductions only a fifth of respondents answered correctly.

The question regarding what people are most concerned about in relation to saving for retirement also revealed that the respondents do not really understand pension reform. Most are concerned that the retirement company will go bankrupt or that they will be defrauded of their money. One of the main changes that pension reform has introduced is separation of the property of participants in saving from company property. It is also interesting that people trust companies managing the third pillar of the pension system, but their trust in the second pillar is minimal. They do not realise that in both cases the same management company is involved.

According to the survey participation in the second pillar is being considered by around 9% of people of active age. In absolute expression this represents about 650,000 people. Now that the sales results for the first half of the year are known and the second pillar has also been opened for people over the age of 35 there are really only just over 77,000 participants in it.

Where is the mistake? The entire reform has been negatively affected by a strong campaign waged against it by the most powerful opposition party. Ever since pension reform began the opposition has stated repeatedly that its post-election priority (following the collapse of former Prime Minister Petr Nečas’ government and early elections called for the Czech Republic in October) will be cancellation of the second pillar of pension reform. Participants in it will reportedly be able to withdraw their savings or transfer them to the third pillar. The expected winner of the elections the Czech Social Democratic Party intends to support it in the future. It plans for example to do more to motivate companies to contribute to their employees’ savings. Whether or not the new government will find a recipe for a satisfactory solution for the ageing population and the dramatic worsening demographics of the Czech Republic’s population in the forthcoming period remains to be seen.

Explore more articles in the Investing category