“Monitoring the pulse of the City Jobs Market”

City Job Market Sees Significant Growth

Job availability in the City up 15% month-on-month

Active jobseekers in the City up 15% month-on-month

London Employment Monitor June 2014 highlights:

- Job vacancies jumped 15% between May 2014 and June 2014

- Year-on-year figures show 10% uplift in available roles

- Candidate numbers increased 15% month-on-month following two previous monthly falls

- Salaries were on average 14% higher for those securing new positions in June 2014

Recruitment Trends and Market Recovery

City recruitment on rebound following hiring dip

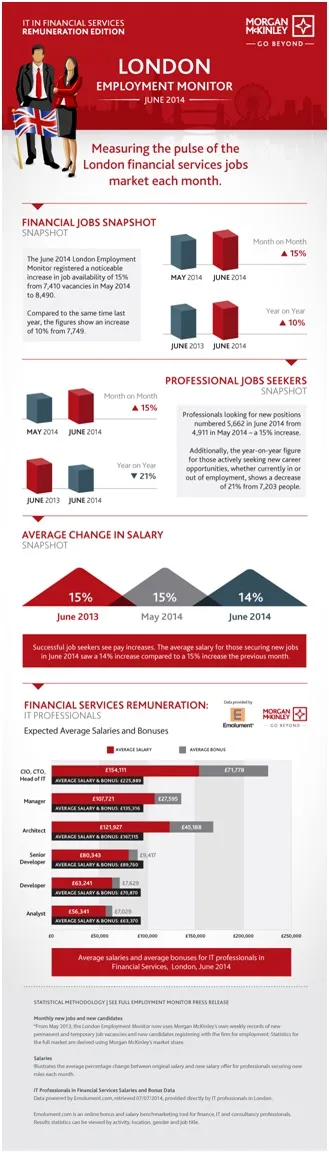

The June 2014 London Employment Monitor shows that City recruitment is back on track again following its May dip, with the number of available roles up 15% in June to 8,490, from 7,410 recorded the previous month. Yearly figures also indicate that hiring continues to move in a positive direction, with job opportunities up 10% in June compared to the same month in 2013, when there were 7,749 roles registered.

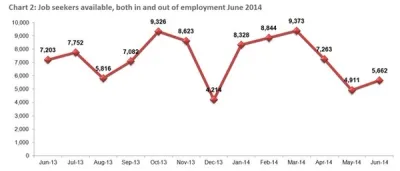

On the candidate side, the market has rallied month-on-month, from 4,911 job seekers in May to 5,662 in June – a rise of 15%. Yearly data shows a 21% decrease in candidate numbers in June compared to the same month last year, as the sector recovers from the impact of two consecutive dips in April and May – the result of four bank holidays and individuals taking extended leave due to the school half-term.

Hakan Enver, Operations Director, Morgan McKinley Financial Services, commented:

“This latest data indicates City hiring is bouncing back following two consecutive months of contraction, which follows our prediction that the market would pick up once the holiday season was over. June saw a 15% leap in the number of roles available, despite conflicting reports from other recruiters in the financial services sector that jobs movement is falling. The positive annual growth figure of 10% is in keeping with the recent CBI/PwC survey, showing UK financial services continue to enjoy an improving outlook, with economic growth stimulating confidence, demand and volumes of business. Within the City, there’s been a renewed appetite for risk, with the IPO and M&A advisory markets currently experiencing a frenzy of activity. This is backed up by news last month that private equity backed flotations reached their highest ever level.

“This positive sentiment has been borne out by a shift in the number of contractor versus permanent placements. During H1 of 2014, there was a 5% increase in permanent vacancies over the period. Year-on-year comparisons show that the volumes increased by 4%. Although the overall flow of opportunities is still in favour of contractors, it is clear to see that the market is increasing its commitment to investing in long-term staff.

“In terms of the functions driving jobs growth, in June we saw a huge amount of activity within the operations and finance sectors. From an operations perspective, there was a notable rise in the number of client services jobs released, seemingly coupled with a rise in demand for portfolio analysts. With high levels of trading activity and increasingly lean and automated middle office functions and processes, client service and portfolio analysts were needed across the board to handle the extra volume.

“Similarly, within accountancy and finance, there has been a considerable focus on recruiting at the AVP level. Qualified accountants with 2 to 5 years’ experience in banking have been in high demand, particularly within product control, regulatory control and financial control.

“Hiring is also buoyant within financial services IT, where an increase in data and software development projects has led to a consistent demand for graduate developers, in particular second jobbers with excellent grades from the Russell Group universities. More specifically, candidates with degrees in engineering, mathematics and computer science who have worked within data rich environments such as financial services, telecoms, software or tech start-ups are highly sought after – even if only with experience in an internship – which is in turn pushing up entry level salaries.

“On the candidate side, as predicted job seeker numbers gathered momentum once again in June, with a 15% month-on-month increase. Looking at the annual drop of 21% in candidate numbers, it’s worth noting that we’re still playing catch-up following the seasonal dips in April and May caused by the spate of spring bank holidays. While there are still pockets of individuals who are putting their job search on hold for the summer, by September we expect the candidate market to have recovered to previous levels seen earlier this year.”

Salaries and Compensation Insights for June

Salaries up by 14% but employers advised to consider more than remuneration to draw talent

The average salary increase for those securing new jobs in June 2014 was 14%, compared to 15% in May 2014.

Enver continued:

“Recent data from REC/KPMG indicating companies are pushing up salaries to attract potential employees echoes are own findings, which reveal salaries increased by 14% in June. Over the last 12 months however, this shows an average increase of 18%. As we reported last month, there’s a high level of competition among employers to attract candidates with niche skill sets, while businesses are doing their utmost to ensure employees stay put by increasing their base pay. However, as the REC/KPMG report also flagged up, remuneration alone is often not sufficient to tempt individuals away from their current position.

IT Sector Salary Gains Highlighted

“In terms of the buoyant IT sector within financial services, Emolument data (Chart 4) shows budding developers are experiencing the greatest remuneration gains, with salaries for the brightest entry-level individuals increasing by 25% since 2008 from circa £45,000 to £56,341 today. This highlights the value of and urgent need for such individuals. Elsewhere, big salaries remain for the top cats in technology, although at other levels, compensation has remained relatively flat for the past five years. For example, while the average CTO earns a healthy £154,111 at a financial institution, this remains exactly the same as in 2007.”

Chart 3: Average change in salary each month June 2014

Chart 3: Average change in salary each month June 2014

Chart 4: Average salary and average bonuses for IT Professionals in Financial Services, London, June 2014

Chart 4: Average salary and average bonuses for IT Professionals in Financial Services, London, June 2014

Methodology Behind London Employment Monitor

Statistical methodology

Statistical methodology

Monthly new jobs and new candidates

*From May 2013, the London Employment Monitor now uses Morgan McKinley’s own weekly records of new permanent and temporary job vacancies and new candidates registering with the firm for employment. Statistics for the full market are derived using Morgan McKinley’s market share.