Business

How high-net-worth families are hedging geopolitical and financial risk through second citizenship

Published by Barnali Pal Sinha

Posted on April 7, 2026

5 min readLast updated: April 7, 2026

Add as preferred source on Google

Published by Barnali Pal Sinha

Posted on April 7, 2026

5 min readLast updated: April 7, 2026

Add as preferred source on GoogleBy Lyle Julien

Investors from the US, the UK, and Canada increasingly look beyond market volatility to where their legal rights, mobility, and access to financial systems are anchored.

While markets move in cycles, rules, borders, and compliance frameworks can change far more abruptly. For high-net-worth families, reliance on a single passport can create an unexpected point of exposure.

This shift explains why second citizenship through established investment programmes is now part of long-term risk planning, alongside portfolio diversification and asset protection.

Investment portfolios spread financial risk across markets, currencies, and instruments, but legal rights work differently. Rights are tied to a person, not to assets, so families can invest globally while still depending on one state for residence, entry, and basic legal protection. This creates a gap between how wealth is diversified and how rights are anchored.

Financial institutions respond by assessing people rather than portfolios. Banks, brokers, and payment providers apply compliance rules to an individual’s legal profile, and citizenship often affects how clients are classified. Even transparent wealth can face delays if a person’s legal status triggers higher scrutiny.

Mobility has become more procedural. For investors from the US, the UK, and Canada, borders are generally open, but travel and relocation can involve more checks and documentation. Secondary screening and additional questions at entry can delay travel, while residence permits and family relocation may require extensive paperwork and can take longer to process.

A simple comparison helps. Diversifying investments is like spreading cargo across several ships, while legal status is the port those ships depend on. If access to that port is restricted, the ships may struggle to operate regardless of how well the cargo is distributed.

Second citizenship works much like a financial hedge because it preserves the ability to act when conditions change. Citizenship by investment programmes offer a regulated way to secure a second legal anchor, reducing reliance on a single framework and adding legal optionality when policies tighten.

The optionality matters because many of today’s risks are sovereign in nature. Governments adjust tax rules, reporting standards, sanctions regimes, and capital controls in response to wider pressures, reshaping how wealth is managed in practice. These decisions are rarely aimed at specific individuals, yet they directly affect access, mobility, and financial continuity.

As oversight increases, regulatory pressure has also risen across developed economies. In some countries, compliance requirements now run deeper through banking, investment, and immigration systems, making preparation and clear structure more important than before.

Timing also matters. Families who plan early usually face fewer constraints, while applications submitted during periods of heightened tension tend to move more slowly and attract greater scrutiny.

It is important to understand that second citizenship has clear limits. It does not remove tax obligations, override international law, or guarantee access to financial institutions. Its value lies in added legal optionality and reduced dependence on a single jurisdiction when conditions change.

High-net-worth families approach second citizenship much like any other structural decision. Marketing claims matter less than credibility, clarity, and long-term viability. The focus is on whether a framework will still function as expected years later.

When evaluating a second citizenship route, investors usually consider several factors:

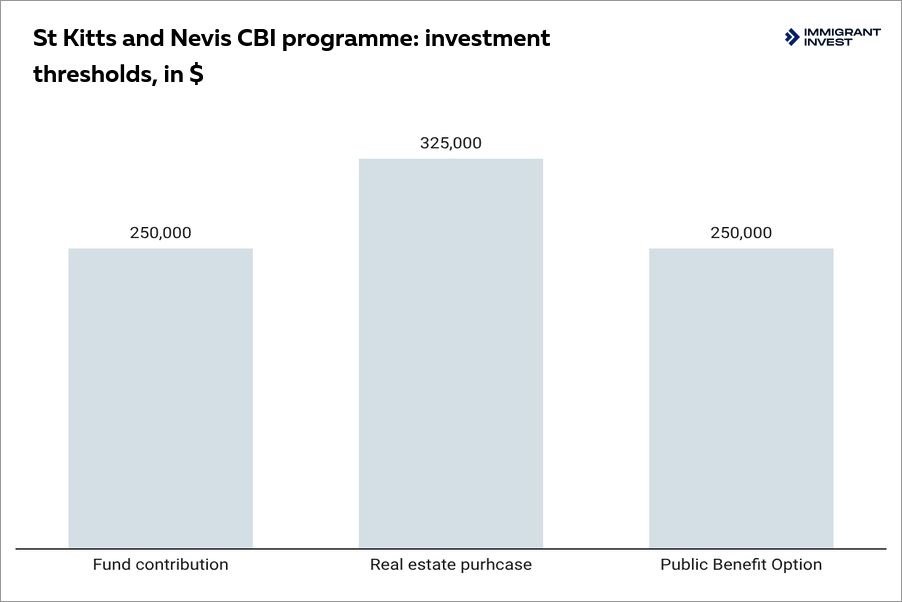

St Kitts and Nevis is often cited as one of the longest-running citizenship by investment frameworks, operating continuously since 1984. In a sector where programmes are frequently paused or revised, this longevity reflects institutional experience and an ability to adapt through economic cycles and periods of increased global scrutiny.

The framework operates in line with international compliance standards. Applications must be submitted through licensed agents and undergo structured Due Diligence, including criminal record checks, source-of-funds verification, and mandatory interviews for adult applicants.

Investment is made through defined routes, such as a government contribution or approved real estate. Clear entry options and documented procedures help investors assess requirements and timelines in advance.

For investors, this structure matters more than speed. Fixed thresholds, standardised documentation, and procedural steps such as approval in principle before funds are transferred reduce uncertainty while strengthening credibility.

The broader lesson is that citizenship by investment works best as part of a regulated and durable system, where continuity and institutional design provide a more reliable basis for long-term planning.

Most risks associated with CBI programmes are operational rather than conceptual. Weak documentation, inconsistent disclosures, or unrealistic expectations can lead to delays, refusals, or reputational risk.

Because applications must be submitted through licensed agents, professional oversight is essential. Aligning applications with compliance standards, preparing source-of-funds documentation, and managing timelines realistically reduces friction, while coordination with tax and banking considerations prioritises predictability over speed.

In this context, companies such as Immigrant Invest operate with a compliance-first approach and focus on documentation quality and Due Diligence execution rather than speed.

Explore more articles in the Business category