Trading

European Credit: More Trouble Ahead

Published by Gbaf News

Posted on April 19, 2012

10 min readLast updated: January 22, 2026

Add as preferred source on Google

Published by Gbaf News

Posted on April 19, 2012

10 min readLast updated: January 22, 2026

Add as preferred source on GoogleA survey of bank risk professionals shows a troubling picture of consumer and small business credit health

By Mike Gordon, FICO

With all the focus on the macroeconomic troubles plaguing Europe, it’s easy to forget about the microeconomic troubles — the problems consumers and small businesses have paying their bills in the midst of a turbulent economy. For credit risk managers at banks across the region, these problems appear to be growing.

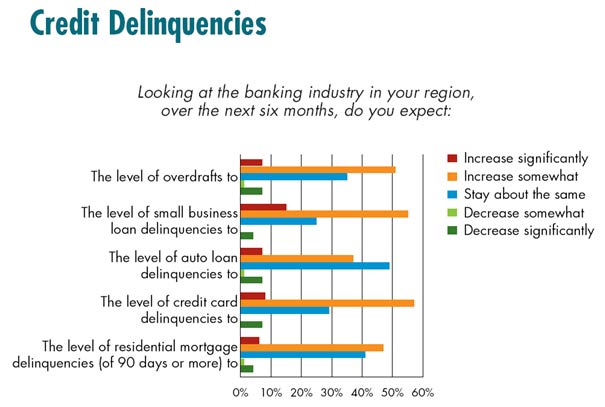

The problem is laid bare in the most recent European Credit Risk Outlook released by FICO, a leading provider of predictive analytics and decision management technology, and the European organization Efma. According to more than 100 European risk professionals surveyed in January and February, consumers and small businesses are going to find it harder to pay back credit of nearly every sort in the coming six months.

The forecast for credit delinquencies was worse across all credit products than in FICO and Efma’s last survey, conducted in fall 2011. Here are some of our top findings:

The rise in small business delinquencies is a particular cause for concern. It’s a sharp increase from FICO and Efma’s last survey, where 52 percent of risk managers predicted credit quality deterioration. In the UK, the percentage of respondents that see an increase in small business loan delinquencies for the next six months jumped from 33 percent in the last survey to 61 percent. In Spain and Portugal, all respondents forecast an increase in delinquencies. The one bright spot was in Germany, Austria and Switzerland, where just 9 percent of respondents forecast an increase.

Now back to the macroeconomy – credit problems reflect not just difficulties for consumers, small businesses and their creditors, but also for the economy overall. For example, when credit card delinquencies rise, card issuers will frequently reduce credit limits to reduce exposure, thus removing credit from the system and indirectly threatening retail sales. When small businesses can’t pay their bills, banks become less willing to lend to other small businesses, which crimps the economy and muffles job creation. Indeed, in our survey, 71 percent of respondents say that small businesses will find it harder to get credit in 2012.

The poor outlook for credit payments reflects a continuation of the vicious cycle that started with the global credit crisis: Credit problems reduce credit supply, which stalls economic recovery, which creates credit problems.

There are other factors straining credit supply right now as well. 68 percent of respondents reported that government deficit reduction measures will reduce bank’s profitability, which again causes banks to protect rather than lend capital. An even higher percentage, 78 percent, say that banking regulations will reduce credit availability. It certainly appears that regulations designed to keep the banking system from overheating are also delaying the thaw.

Furthermore, 55 percent of respondents said major banks will reduce their operations in Central and Eastern Europe, a trend that was just beginning to materialize in late 2011. Exposure in Central and Eastern Europe creates a need for the banks to hold more capital and, as capital is scarce, the normal reaction will be reduce exposure. However, credit demand in this region is still growing, and it can be more profitable for lenders to keep lending here, if they can cover the capital needs.

Where are things looking up? First, in the DACH region – Germany, Austria and Switzerland. The relative strength of these economies extends to consumers and small businesses, and lenders there were considerably more sanguine about the rest of the year.

For more economic good news, cross the pond. The responses to FICO’s latest survey in the U.S., conducted with PRMIA, shows a strong upward trend in optimism.

With delinquencies rising and regulations tightening, what’s the game plan for European lenders? The challenges facing banks boil down to two overarching disciplines – capital management and risk management. Knowing where a bank stands today on these two measures will tell you what their strategic priorities will be for 2012.

Despite more stringent spending reviews, banks will invest in making sure their risk management teams, systems and processes for each product category are sound enough to enable responsible lending growth. They will also look for ways to make sure lending decisions are in synch with their capital management strategy, so that they neither increase the capital burden to an unsustainable level nor choke off profitable lending that could provide a strong return on capital.

Neither small businesses nor consumers are going to find their credit load easy to bear this year. But banks that excel at risk management and capital management will use this time to increase their lead in the market.

Mike Gordon is vice president and general manager for Europe, the Middle East and Africa at FICO. For a copy of the latest European Credit Risk Outlook, visit www.fico.com/news.

Source: European Credit Risk Outlook, March 2012. Copyright 2012 Fair Isaac Corporation.

A survey of bank risk professionals shows a troubling picture of consumer and small business credit health

By Mike Gordon, FICO

With all the focus on the macroeconomic troubles plaguing Europe, it’s easy to forget about the microeconomic troubles — the problems consumers and small businesses have paying their bills in the midst of a turbulent economy. For credit risk managers at banks across the region, these problems appear to be growing.

The problem is laid bare in the most recent European Credit Risk Outlook released by FICO, a leading provider of predictive analytics and decision management technology, and the European organization Efma. According to more than 100 European risk professionals surveyed in January and February, consumers and small businesses are going to find it harder to pay back credit of nearly every sort in the coming six months.

The forecast for credit delinquencies was worse across all credit products than in FICO and Efma’s last survey, conducted in fall 2011. Here are some of our top findings:

The rise in small business delinquencies is a particular cause for concern. It’s a sharp increase from FICO and Efma’s last survey, where 52 percent of risk managers predicted credit quality deterioration. In the UK, the percentage of respondents that see an increase in small business loan delinquencies for the next six months jumped from 33 percent in the last survey to 61 percent. In Spain and Portugal, all respondents forecast an increase in delinquencies. The one bright spot was in Germany, Austria and Switzerland, where just 9 percent of respondents forecast an increase.

Now back to the macroeconomy – credit problems reflect not just difficulties for consumers, small businesses and their creditors, but also for the economy overall. For example, when credit card delinquencies rise, card issuers will frequently reduce credit limits to reduce exposure, thus removing credit from the system and indirectly threatening retail sales. When small businesses can’t pay their bills, banks become less willing to lend to other small businesses, which crimps the economy and muffles job creation. Indeed, in our survey, 71 percent of respondents say that small businesses will find it harder to get credit in 2012.

The poor outlook for credit payments reflects a continuation of the vicious cycle that started with the global credit crisis: Credit problems reduce credit supply, which stalls economic recovery, which creates credit problems.

There are other factors straining credit supply right now as well. 68 percent of respondents reported that government deficit reduction measures will reduce bank’s profitability, which again causes banks to protect rather than lend capital. An even higher percentage, 78 percent, say that banking regulations will reduce credit availability. It certainly appears that regulations designed to keep the banking system from overheating are also delaying the thaw.

Furthermore, 55 percent of respondents said major banks will reduce their operations in Central and Eastern Europe, a trend that was just beginning to materialize in late 2011. Exposure in Central and Eastern Europe creates a need for the banks to hold more capital and, as capital is scarce, the normal reaction will be reduce exposure. However, credit demand in this region is still growing, and it can be more profitable for lenders to keep lending here, if they can cover the capital needs.

Where are things looking up? First, in the DACH region – Germany, Austria and Switzerland. The relative strength of these economies extends to consumers and small businesses, and lenders there were considerably more sanguine about the rest of the year.

For more economic good news, cross the pond. The responses to FICO’s latest survey in the U.S., conducted with PRMIA, shows a strong upward trend in optimism.

With delinquencies rising and regulations tightening, what’s the game plan for European lenders? The challenges facing banks boil down to two overarching disciplines – capital management and risk management. Knowing where a bank stands today on these two measures will tell you what their strategic priorities will be for 2012.

Despite more stringent spending reviews, banks will invest in making sure their risk management teams, systems and processes for each product category are sound enough to enable responsible lending growth. They will also look for ways to make sure lending decisions are in synch with their capital management strategy, so that they neither increase the capital burden to an unsustainable level nor choke off profitable lending that could provide a strong return on capital.

Neither small businesses nor consumers are going to find their credit load easy to bear this year. But banks that excel at risk management and capital management will use this time to increase their lead in the market.

Mike Gordon is vice president and general manager for Europe, the Middle East and Africa at FICO. For a copy of the latest European Credit Risk Outlook, visit www.fico.com/news.

Source: European Credit Risk Outlook, March 2012. Copyright 2012 Fair Isaac Corporation.

Explore more articles in the Trading category