Nikkei 225 futures, and in particular CME’s Nikkei 225 futures, have experienced significant growth during 2013, motivated by optimism for the Japanese economic outlook. To help equity market participants take advantage of this changing Japanese economic landscape CME Group will introduce both quarterly and serial options on Yen Denominated Nikkei Stock Average futures on CME Globex beginning at 5PM on January 12, 2014 for trade date January 13, 2014.

CME Group

Impact of Abenomics on Nikkei 225 Market

“Abenomics” has been the recent catalyst for increased activity in Japanese cash equity market and Japanese equity derivative market activity. Abenomics refers to the economic policies implemented in Japan under the direction of Prime Minister Shinzo Abe. The three pronged approach of Abenomics includes – monetary stimulus; fiscal stimulus; and, structural reforms. The intent of Abenomics is to jumpstart Japanese economic growth, which has been quite lackluster since the late 1980s.

It is an understatement to indicate that the Japanese equity market has reacted very favorably to Abenomics. The Nikkei 225 index, Japan’s premier equity market index, rallied more than 50% from December 28 2012 through the closing level posted on May 22, 2013. Subsequently, the Nikkei 225 declined more than 20% from late May 2013 through mid-June 2013, before recovering substantively. As of November 8, 2013, the Nikkei 225 index has appreciated slightly more than 35.5%. This price pattern is illustrated in the Nikkei 225 Index chart below:

nikkei225

Analyzing Volatility in Japanese Equities

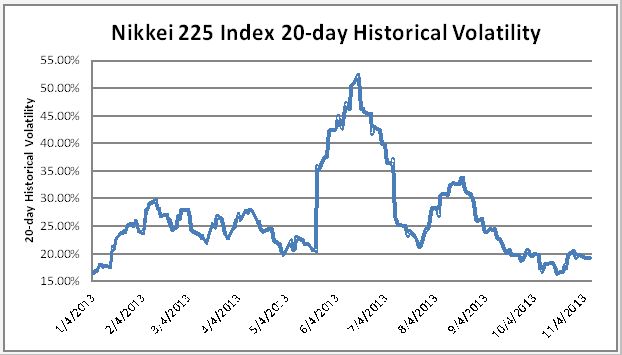

An alternative way of viewing the recent heightened Japanese equity market price volatility is through the lens of Nikkei 225 Index 20-day historical volatility (20-day HV). During late 2012, the range for Nikkei 225 20-day HV lingered in the 12% to 16% range. The strong early 2013 Japanese equity market rally propelled 20-day HV into the 20% to 30% range. Historical volatility exploded along with the Nikkei 225’s strong price declines in late May/early June 2013, peaking near 52%, before reverting back towards the recent 20% level. The historical volatility pattern is shown in the Nikkei 225 Index 20-day Historical Volatility chart below:

nikkei225

A significant increase in Nikkei 225 futures trading activity has coincided with the recovery in the Japanese equity market and the increase in realized volatility. Trading volume in CME’s Yen Denominated Nikkei 225 futures has increased more than 100% to nearly 47,000 contracts per day during the first ten months of 2013, while Nikkei 225 futures volume at the Osaka Securities Exchange has increased more than 77% during the same time period.

Demand for Options on Nikkei 225 Futures

This substantial Nikkei 225 futures volume trend has created demand for options on Nikkei 225 futures, a contract that CME has introduced which can be cleared at CME. Japanese equity market participants have been seeking an alternative method of gaining exposure to the equity market price shifts. The introduction of CME options on Nikkei 225 futures gives traders an enhanced set of tools by which they can establish market exposures than can’t be accomplished with futures contracts alone.

The potential options on futures strategies that may be used include, but are not limited to: limited risk price directional positions associated with long option exposure and/or debit vertical spread exposure; long or short volatility trading positions via traditional straddle or strangle positions; income enhancement positions via covered option writing programs;, time value capture related positions via butterfly, condor or horizontal spreads; as well as dynamic portfolio reweighting programs via strangle writing strategies.

Launch Details for CME Nikkei 225 Options

CME will introduce options on Yen Denominated Nikkei Stock Average futures on CME Globex beginning at 5PM on January 12, 2014 for trade date January 13, 2014.

CME options on Yen Denominated Nikkei futures will be listed on 2 quarterly cycle months (March/June/September/December) and 2 serial months (January/February/April/May/July/August/ October/November) listed at any time. The cycle month options will feature American-style exercise, whereas the serial month options will feature European-style exercise.

Serial month options will be automatically exercised into CME Yen Denominated Nikkei futures based on a fixing price determined by trading activity in the mini Nikkei futures at the Osaka Securities Exchange (OSE) during the last thirty seconds of cash equity market trading on the serial option expiration day. Contrarian instructions are not permitted for serial options on CME’s Yen Denominated Nikkei Stock Average futures.

Quarterly CME Yen Denominated Nikkei Stock Average futures will settle to a Special Opening Quotation (SOQ) of the Nikkei 225 index on the second Friday of the expiration month. In-the-money options on CME’s Yen Denominated Nikkei Stock Average futures are automatically exercised on expiration day into the underlying futures contract, which is then marked to market against the Nikkei 225 Stock Average SOQ.

Risks and Considerations for Investors

Futures and options trading is not suitable for all investors, and involves the risk of loss. Futures and options are a leveraged investment, and because only a percentage of a contract’s value is required to trade, it is possible to lose more than the amount of money deposited for a futures position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles. And only a portion of those funds should be devoted to any one trade because they cannot expect to profit on every trade.

Any research views expressed are those of the individual author and do not necessarily represent the views of the CME Group or its affiliates.

All examples are hypothetical situations, used for explanation purposes only, and should not be considered investment advice or the results of actual market experience.

All matters pertaining to rules and specifications herein are made subject to and are superseded by official CME, CBOT, NYMEX and KCBT rules. Current rules should be consulted in all cases concerning contract specifications.

JOHN NYHOFF

About the Author:

JOHN NYHOFF

Executive Director, Financial Research and Product Development

John Nyhoff serves as Executive Director, Financial Research and Product Development of CME Group. He is responsible for developing interest rate and credit-related products. Previously, Nyhoff served as Director, Research and Product Development of CME since March 2006.

Before joining CME, Nyhoff most recently served as Executive Vice President and Co-Chief Operating Officer for Tokyo-Mitsubishi Futures, Inc., the futures subsidiary of Japan’s largest bank. He worked for Tokyo-Mitsubishi since 1988, holding a variety of roles responsible for strategic planning, economic analysis, marketing and electronic trading including Senior Vice President, Trading & Research and Vice President & Chief Economist. He also worked as an Options Specialist for SECTREND, a futures commission merchant that became part of Tokyo-Mitsubishi. Nyhoff also served as Vice President for Refco, Inc. where he was responsible for recruiting new customers to derivatives trading. He began his career as Senior Financial Economist for The Chicago Board of Trade.

Nyhoff earned a bachelor’s degree in economics from DePaul University, a master’s degree in economics from Northern Illinois University and a master’s degree in financial economics from Simon Graduate School of Business at the University of Rochester. He has worked as a business statistics instructor at Northern Illinois University and has co-authored a number of publications, including Trading Options on Futures: Markets, Methods, Strategies & Tactics (John Wiley & Sons, 1988) and Trading Financial Futures: Markets, Methods, Strategies & Tactics (John Wiley & Sons, 1988).

Nikkei 225 futures, and in particular CME’s Nikkei 225 futures, have experienced significant growth during 2013, motivated by optimism for the Japanese economic outlook. To help equity market participants take advantage of this changing Japanese economic landscape CME Group will introduce both quarterly and serial options on Yen Denominated Nikkei Stock Average futures on CME Globex beginning at 5PM on January 12, 2014 for trade date January 13, 2014.

CME Group

“Abenomics” has been the recent catalyst for increased activity in Japanese cash equity market and Japanese equity derivative market activity. Abenomics refers to the economic policies implemented in Japan under the direction of Prime Minister Shinzo Abe. The three pronged approach of Abenomics includes – monetary stimulus; fiscal stimulus; and, structural reforms. The intent of Abenomics is to jumpstart Japanese economic growth, which has been quite lackluster since the late 1980s.

It is an understatement to indicate that the Japanese equity market has reacted very favorably to Abenomics. The Nikkei 225 index, Japan’s premier equity market index, rallied more than 50% from December 28 2012 through the closing level posted on May 22, 2013. Subsequently, the Nikkei 225 declined more than 20% from late May 2013 through mid-June 2013, before recovering substantively. As of November 8, 2013, the Nikkei 225 index has appreciated slightly more than 35.5%. This price pattern is illustrated in the Nikkei 225 Index chart below:

nikkei225

An alternative way of viewing the recent heightened Japanese equity market price volatility is through the lens of Nikkei 225 Index 20-day historical volatility (20-day HV). During late 2012, the range for Nikkei 225 20-day HV lingered in the 12% to 16% range. The strong early 2013 Japanese equity market rally propelled 20-day HV into the 20% to 30% range. Historical volatility exploded along with the Nikkei 225’s strong price declines in late May/early June 2013, peaking near 52%, before reverting back towards the recent 20% level. The historical volatility pattern is shown in the Nikkei 225 Index 20-day Historical Volatility chart below:

nikkei225

A significant increase in Nikkei 225 futures trading activity has coincided with the recovery in the Japanese equity market and the increase in realized volatility. Trading volume in CME’s Yen Denominated Nikkei 225 futures has increased more than 100% to nearly 47,000 contracts per day during the first ten months of 2013, while Nikkei 225 futures volume at the Osaka Securities Exchange has increased more than 77% during the same time period.

This substantial Nikkei 225 futures volume trend has created demand for options on Nikkei 225 futures, a contract that CME has introduced which can be cleared at CME. Japanese equity market participants have been seeking an alternative method of gaining exposure to the equity market price shifts. The introduction of CME options on Nikkei 225 futures gives traders an enhanced set of tools by which they can establish market exposures than can’t be accomplished with futures contracts alone.

The potential options on futures strategies that may be used include, but are not limited to: limited risk price directional positions associated with long option exposure and/or debit vertical spread exposure; long or short volatility trading positions via traditional straddle or strangle positions; income enhancement positions via covered option writing programs;, time value capture related positions via butterfly, condor or horizontal spreads; as well as dynamic portfolio reweighting programs via strangle writing strategies.

CME will introduce options on Yen Denominated Nikkei Stock Average futures on CME Globex beginning at 5PM on January 12, 2014 for trade date January 13, 2014.

CME options on Yen Denominated Nikkei futures will be listed on 2 quarterly cycle months (March/June/September/December) and 2 serial months (January/February/April/May/July/August/ October/November) listed at any time. The cycle month options will feature American-style exercise, whereas the serial month options will feature European-style exercise.

Serial month options will be automatically exercised into CME Yen Denominated Nikkei futures based on a fixing price determined by trading activity in the mini Nikkei futures at the Osaka Securities Exchange (OSE) during the last thirty seconds of cash equity market trading on the serial option expiration day. Contrarian instructions are not permitted for serial options on CME’s Yen Denominated Nikkei Stock Average futures.

Quarterly CME Yen Denominated Nikkei Stock Average futures will settle to a Special Opening Quotation (SOQ) of the Nikkei 225 index on the second Friday of the expiration month. In-the-money options on CME’s Yen Denominated Nikkei Stock Average futures are automatically exercised on expiration day into the underlying futures contract, which is then marked to market against the Nikkei 225 Stock Average SOQ.

Futures and options trading is not suitable for all investors, and involves the risk of loss. Futures and options are a leveraged investment, and because only a percentage of a contract’s value is required to trade, it is possible to lose more than the amount of money deposited for a futures position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles. And only a portion of those funds should be devoted to any one trade because they cannot expect to profit on every trade.

Any research views expressed are those of the individual author and do not necessarily represent the views of the CME Group or its affiliates.

All examples are hypothetical situations, used for explanation purposes only, and should not be considered investment advice or the results of actual market experience.

All matters pertaining to rules and specifications herein are made subject to and are superseded by official CME, CBOT, NYMEX and KCBT rules. Current rules should be consulted in all cases concerning contract specifications.

JOHN NYHOFF

About the Author:

JOHN NYHOFF

Executive Director, Financial Research and Product Development

John Nyhoff serves as Executive Director, Financial Research and Product Development of CME Group. He is responsible for developing interest rate and credit-related products. Previously, Nyhoff served as Director, Research and Product Development of CME since March 2006.

Before joining CME, Nyhoff most recently served as Executive Vice President and Co-Chief Operating Officer for Tokyo-Mitsubishi Futures, Inc., the futures subsidiary of Japan’s largest bank. He worked for Tokyo-Mitsubishi since 1988, holding a variety of roles responsible for strategic planning, economic analysis, marketing and electronic trading including Senior Vice President, Trading & Research and Vice President & Chief Economist. He also worked as an Options Specialist for SECTREND, a futures commission merchant that became part of Tokyo-Mitsubishi. Nyhoff also served as Vice President for Refco, Inc. where he was responsible for recruiting new customers to derivatives trading. He began his career as Senior Financial Economist for The Chicago Board of Trade.

Nyhoff earned a bachelor’s degree in economics from DePaul University, a master’s degree in economics from Northern Illinois University and a master’s degree in financial economics from Simon Graduate School of Business at the University of Rochester. He has worked as a business statistics instructor at Northern Illinois University and has co-authored a number of publications, including Trading Options on Futures: Markets, Methods, Strategies & Tactics (John Wiley & Sons, 1988) and Trading Financial Futures: Markets, Methods, Strategies & Tactics (John Wiley & Sons, 1988).