Technology

Basel IV vs. The AI Bots: Why the Banking Rulebook Must Evolve in the Age of Algorithmic Herding

Published by Barnali Pal Sinha

Posted on April 8, 2026

8 min readLast updated: April 8, 2026

Add as preferred source on Google

Published by Barnali Pal Sinha

Posted on April 8, 2026

8 min readLast updated: April 8, 2026

Add as preferred source on GooglePhoto credit: Jim Howel

By Angelica Burlaza

The next financial crisis may not trigger a bank run, but a code run. As algorithms synchronize, borders close, and the global workforce stagnates, the margin for error in the global economy is vanishing.

Sitting down with Dr. Eric Balki in a London office feels less like a typical interview and more like witnessing a glimpse into a future where the foundations of the global economy are shifting. The conversation captures one of the most distinctive perspectives on how AI, human productivity, demographics, longevity, and banking regulation are about to collide and ultimately redefine how economies function.

As a founder of a diverse group of businesses, Dr. Balki operates at the intersection of longevity science, healthcare, and deep-tech infrastructure. It is a vantage point that has led him to a stark conclusion: the global financial regulatory framework is slowly drifting out of sync with the reality of modern markets. Dr. Balki’s warning carries unusual weight because he is not a mere outside observer guessing at the technology; he is an insider who helped build it. An early innovator in AI and supercomputing, working in the North East of England, he developed some of the early models for Natural Language Processing (NLP), long before “generative AI” became a household term.

A multidisciplinary academic background matches Dr. Balki’s technical expertise. He holds degrees in Physics, Finance, and Management from King’s College London and Lancaster University, as well as a PhD in Aging and Longevity, during which he also serves as an Honorary Research Fellow, heading a lab conducting cutting-edge research. This combination of complex physics, finance, and systems thinking in healthcare allows him to see the “wiring” of the system that others might miss.

With the focus of this discussion on banking regulatory environments, his assessment centers on Basel, the venerable international accord that dictates how banks manage capital and measure risk. Since the 2008 financial crisis, Basel has served as a firewall for the global economy, designed to absorb shocks and prevent one institution’s failure from infecting the whole.

But Dr. Balki argues that AI is changing the fundamental physics of risk.

“We are entering a period where algorithms direct capital flows in picoseconds,” he says. “Yet our regulatory system still relies on human-paced decision-making and retroactive reporting. There is a growing latency gap between how fast the market moves and how fast our oversight can react.”

The Speed Mismatch

Basel was designed for a world where risk accumulated slowly. Bad loans festered over the years, leverage crept up over the quarters, and regulators used systems that looked at balance sheets, often to see what had already happened.

AI compresses this timeline. A modern, AI-native institution ingests signals, reprices risk, and continuously shifts exposure. Risk is no longer a static item on a ledger; it is a live, adaptive system.

“The issue isn’t that Basel isn’t a great idea; it actually is critical to financial systems,” Dr. Balki clarifies. “Basel protects against solvency crises, running out of money. It needs to evolve for speed crises, running out of time.”

The New Threat: Algorithmic Herding

The danger, according to Dr. Balki, is not that an AI will make a mistake; it is that thousands of AIs will make the same mistake at the same time. In a market dominated by machine learning, institutions often optimize for similar objectives and use similar datasets. This creates a hidden correlation. When a shock hits, these models may simultaneously decide to deleverage, exit a sector, or short an asset.

This is algorithmic herding.

When herding happens at machine speed, liquidity does not just thin; it evaporates. Prices don’t just fall; they gap.

“A static capital buffer doesn’t stop a synchronized, machine-speed sell-off,” he warns. “Humans end up trying to manage a crisis that was effectively decided before a committee meeting to discuss it was called to order.”

The Macro Trap: The Aging-Productivity Squeeze

Dr. Balki’s argument takes a darker turn when he zooms out to the macroeconomic landscape, a perspective informed by his research in longevity. He believes this regulatory blind spot is colliding with an irresistible demographic force.

Across advanced economies, the math of growth is breaking. As populations age, the labor force shrinks, leaving fewer workers to support a growing pool of retirees.

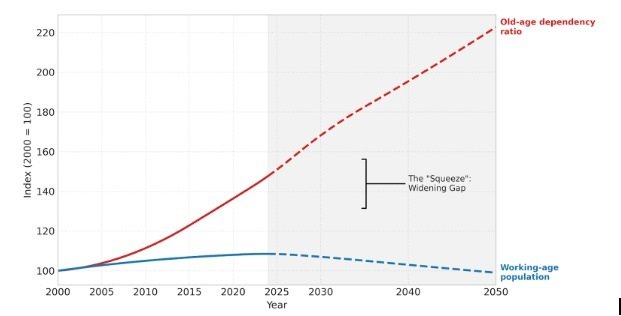

The data paints a clear, two-track picture of this deepening crisis:

Figure 1: The chart above visualizes the "Aging-Productivity Squeeze" using data for advanced economies (proxied by the High-Income Countries aggregates from the UN and the World Bank). Courtesy Dr. Eric Balki’s Longevity Lab.

The Divergence: The Old-Age Dependency Ratio is projected to more than double relative to 2000 levels. The burden on the working population is becoming mathematically unsustainable under current models.

The Stagnation: Simultaneously, the working-age population has effectively peaked. In many G7 nations, it is projected to stagnate or decline through 2050, creating a permanent labor supply constraint.

“This creates a ‘squeeze’ on economic growth,” Dr. Balki explains. “To maintain the standard of living we are used to, GDP growth of 2% or 2.5%, while the workforce shrinks, we cannot just work harder. We need to work radically smarter. Perhaps AI can help with this, but it also has potentially large negative consequences on people's lives that we need to be wary of.”

The Geopolitical Friction: Borders and Tariffs

Dr. Balki points out that just as demographics are tightening the labor supply, politics are seizing up the remaining gears of mobility.

“For decades, global labor mobility acted as a pressure-release valve,” he notes. “When one region lacked workers, migration helped fill the gap, and capital flows also helped. But rising anti-immigration rhetoric in Western economies is effectively freezing this mechanism.” He views the return of tariff wars and protectionism as a similar regression. The dismantling of the cross-border efficiencies that have sustained GDP growth and global order for the last thirty years is exacerbating the very stagnation they are trying to fight.

“We are building walls around shrinking pools of labor,” Dr. Balki says. “While it appears to give an illusion of sovereignty, it may very well just be that, a magician’s trick, just an illusion, making markets less competitive, and the labor workforce less productive.”

The Compliance Paradox

Compounding these pressures is a regulatory environment that Dr. Balki describes as increasingly difficult for businesses. The burden of compliance increased on businesses, leaving little breathing room to innovate, especially in Europe. Such a burden is less pronounced in rapidly advancing economies like China, which have begun to outpace the technological revolution.

Change to:

Compounding these pressures is a regulatory environment that Dr. Balki describes as increasingly complex for businesses to navigate. Rising compliance demands are consuming greater time and resources, often leaving less room for innovation—particularly in parts of Europe. By contrast, some rapidly advancing economies have adopted more adaptive regulatory approaches, enabling faster technological development and, in certain areas, gaining momentum in the broader innovation landscape.

“Companies are spending significant capital just to prove they are following the rules, rather than finding new ways to grow,” he argues. “When you spend a significant portion of your time on compliance, and an ever more complex tax landscape, you cannot make the productivity gains necessary to offset the demographic decline.”

In the age of AI, he fears this dynamic will worsen. If regulators respond to the technology with heavy-handed, bureaucratic frameworks, they risk stifling one major tool capable of solving the productivity crisis.

“The irony,” Dr. Balki warns, “is that the regulations designed to prevent a crisis may very well drive businesses towards one.”

“Basel V?”: An Algorithmic Accord

This is why Dr. Balki is calling for a new approach. He suggests a framework that moves beyond static capital requirements to monitor the diversity and behavior of the code running the financial system. It would prioritize resilience and speed over bureaucracy, while also making systems less opaque and better protecting citizen privacy.

“If we don’t build a framework that speaks the language of the technology driving markets,” he concludes, “we risk more than just another financial crisis. This time, the tools at our disposal to limit the damage, such as money supply, quantitative easing, and interest rate adjustments, may very well have little to no immediate impact. Furthermore, privacy and freedoms need to be protected in this new age, where we can have a runaway effect, where technology can, in effect, completely run most people’s lives, with them having little to no say.”

Change to:

“If the regulatory framework does not evolve to match the speed and behavior of AI-driven markets, the next financial crisis may unfold faster than institutions are able to react—making adaptability, not just stability, the defining principle of future oversight.”

Explore more articles in the Technology category