Nearly Five Million Consider Switching Accounts

Research from SAS identifies appetite from consumers to find a new current account provider

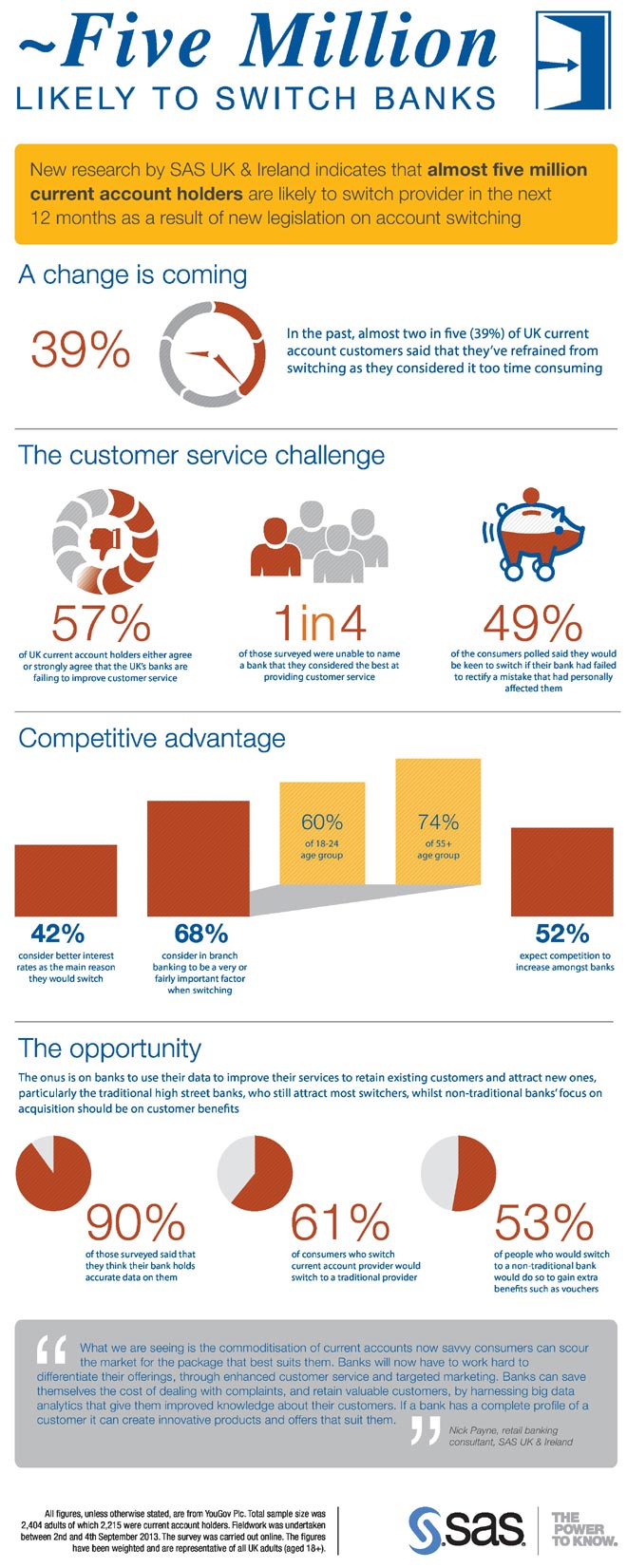

New online research indicates that almost five million[1] current account holders are likely to switch provider in the next 12 months as a result of the new legislation on account switching which comes into force on 16 September. This is the key finding from a detailed investigation into customer service in banking released today by business analytics leader SAS, following independent research by YouGov.

CURRENT ACCOUNT HOLDERS READY TO SWITCH BANKS

Barriers Preventing UK Consumers from Switching

The research also identified that almost two in five (39%) of UK current account holders said that they would refrain from switching current account provider if the process of switching accounts was too time consuming. Under the new account switching rules, consumers will be able to have their current account services transferred between providers in seven working days, with their new provider managing the process on their behalf. This suggests that millions more could be inclined to switch.

UK Banks Struggle with Customer Service

The research also uncovered that 57 per cent of UK current account holders either agree or strongly agree that the UK’s banks are failing to improve customer service. In October 2012 SAS commissioned similar research into customer service in banking and found that 65 per cent of UK adults who were registered with a high street bank believed banks were failing to improve their customer service levels. However, almost one in four (24%) current account holders said they didn’t perceive any bank to be the best at providing customer service.

Banks Possess Customer Data But Must Act

Interestingly, banks appear to have the tools at their disposal to improve services, as 90 per cent of those surveyed said that they think their bank holds accurate data on them. The onus, therefore, is on banks to use this data to improve the services they provide to retain existing customers and attract new ones. This is particularly important for the traditional high street banks as the survey showed that if consumers do switch current account provider, they would be more likely to switch like for like, with over three in five (61%) current account holders saying they would switch to a traditional provider.

Nick Payne, retail banking consultant, SAS UK & Ireland comments: “Historically, consumer churn between retail banks has been between two and three per cent, however our research suggests this could increase significantly. What we are seeing is the commoditisation of current accounts now savvy consumers can scour the market for the package that best suits them. Banks will now have to work hard to differentiate their offerings, through enhanced customer service and targeted marketing. Almost half (49%) of the consumers polled in our survey said they would be more inclined to switch if their bank had failed to rectify a mistake that had personally affected them. Banks can save themselves the cost of dealing with complaints, and retain valuable customers, by harnessing Big Data Analytics that give them improved knowledge about their customers. If a bank has a complete profile of a customer it can create innovative products and offers that suit them.”

Expert Insights on Big Data and Banking

Professor Moira Clark, Henley Business School, authored a paper last year entitled ‘A Single View of the Customer and the emerging role of Big Data’ which focussed on financial services. She says: “These findings suggest that banks are still not perceived as making improvements to customer service quickly. In the past consumers have been generally dissatisfied with their account providers, but have been apathetic to switch as they saw it as risky and complex. With account switching removing the risk and complexity, banks need to invest in IT systems and skilled data analysts, while creating a culture of being customer focused. Improving data quality is fundamental to achieving risk and compliance demands, and will enable banks to deliver a consistent and strong customer experience.”

[1] Figures calculated by SAS based on number of YouGov survey respondents who have UK current account and mid-year population estimates from the ONS.

SAS Account Switch Infograph

Research from SAS identifies appetite from consumers to find a new current account provider

New online research indicates that almost five million[1] current account holders are likely to switch provider in the next 12 months as a result of the new legislation on account switching which comes into force on 16 September. This is the key finding from a detailed investigation into customer service in banking released today by business analytics leader SAS, following independent research by YouGov.

CURRENT ACCOUNT HOLDERS READY TO SWITCH BANKS

The research also identified that almost two in five (39%) of UK current account holders said that they would refrain from switching current account provider if the process of switching accounts was too time consuming. Under the new account switching rules, consumers will be able to have their current account services transferred between providers in seven working days, with their new provider managing the process on their behalf. This suggests that millions more could be inclined to switch.

The research also uncovered that 57 per cent of UK current account holders either agree or strongly agree that the UK’s banks are failing to improve customer service. In October 2012 SAS commissioned similar research into customer service in banking and found that 65 per cent of UK adults who were registered with a high street bank believed banks were failing to improve their customer service levels. However, almost one in four (24%) current account holders said they didn’t perceive any bank to be the best at providing customer service.

Interestingly, banks appear to have the tools at their disposal to improve services, as 90 per cent of those surveyed said that they think their bank holds accurate data on them. The onus, therefore, is on banks to use this data to improve the services they provide to retain existing customers and attract new ones. This is particularly important for the traditional high street banks as the survey showed that if consumers do switch current account provider, they would be more likely to switch like for like, with over three in five (61%) current account holders saying they would switch to a traditional provider.

Nick Payne, retail banking consultant, SAS UK & Ireland comments: “Historically, consumer churn between retail banks has been between two and three per cent, however our research suggests this could increase significantly. What we are seeing is the commoditisation of current accounts now savvy consumers can scour the market for the package that best suits them. Banks will now have to work hard to differentiate their offerings, through enhanced customer service and targeted marketing. Almost half (49%) of the consumers polled in our survey said they would be more inclined to switch if their bank had failed to rectify a mistake that had personally affected them. Banks can save themselves the cost of dealing with complaints, and retain valuable customers, by harnessing Big Data Analytics that give them improved knowledge about their customers. If a bank has a complete profile of a customer it can create innovative products and offers that suit them.”

Professor Moira Clark, Henley Business School, authored a paper last year entitled ‘A Single View of the Customer and the emerging role of Big Data’ which focussed on financial services. She says: “These findings suggest that banks are still not perceived as making improvements to customer service quickly. In the past consumers have been generally dissatisfied with their account providers, but have been apathetic to switch as they saw it as risky and complex. With account switching removing the risk and complexity, banks need to invest in IT systems and skilled data analysts, while creating a culture of being customer focused. Improving data quality is fundamental to achieving risk and compliance demands, and will enable banks to deliver a consistent and strong customer experience.”

[1] Figures calculated by SAS based on number of YouGov survey respondents who have UK current account and mid-year population estimates from the ONS.

SAS Account Switch Infograph