Investing

RISING SPEND ON OVERHEADS WIPING OUT AIM COMPANY PROFITS

Published by Gbaf News

Posted on March 11, 2014

4 min readLast updated: January 22, 2026

Published by Gbaf News

Posted on March 11, 2014

4 min readLast updated: January 22, 2026

But directors silent in annual reports on rising running costs

Research into the accounts of 134 AIM-listed companies by accountancy firm SKS Business Services reveals a surprising leap in spend on non-core operations that has more than wiped out their profits[i] over the past 5 years. Findings include:

The in-depth study of 670 small-cap financial reports[ii] shows that costs relating to non-core operations such as finance, legal and rents have soared 21 per cent in the last five years from £4.53m in 2008 to £5.47m in 2012, while profits over this time have fallen from an average of £9.6 million to an average loss of £1.52 million last year.

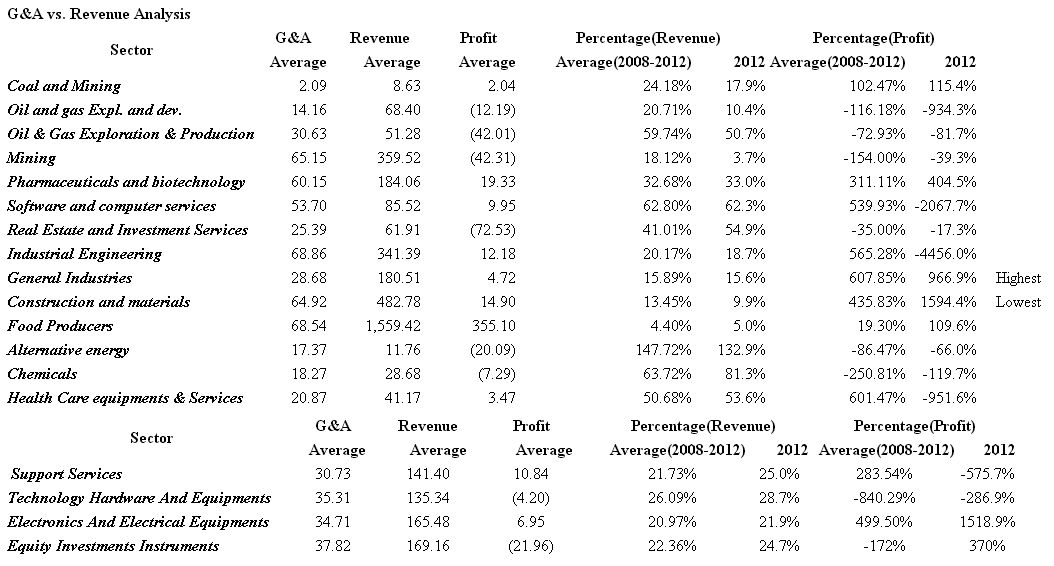

Firms operating in alternative energy and chemicals spend the greatest portion of their revenue on General & Administrative (G&A) expenses, while food producers and construction companies have their non-core operational costs most in check.

Firms operating in alternative energy and chemicals spend the greatest portion of their revenue on General & Administrative (G&A) expenses, while food producers and construction companies have their non-core operational costs most in check.

SKS expected to find that high investment sectors, such as energy and chemicals, will have high G&A spend as they need the support infrastructure to develop their products, while traditional sectors will have developed efficiencies and have their non-core costs in check. However, overall and across all sectors, the research shows that head office costs are going up disproportionately.

Of 134 of the Aim-listed companies, only three have management discussion and analysis (MD&A) reports – in other words barely 2% of AIM companies, a very surprisingly low amount. In these three reports, G&A is only mentioned with regards to an increase in costs, rather than in terms of any plans to reduce it.

Sanjay Swarup, Director, SKS Business Services, said: “Although AIM-listed companies are not required to produce MD&A reports, their absence and the increases in costs in this area suggests that overhead and administration costs are not being properly managed at many.

“Regardless of the general upward trend of costs caused by compliance and regulatory matters, the past few years presented the opportunity to cut costs through better use of technologies and generally negotiate better terms with suppliers. This has not been the case and, in particular, there is compelling evidence here of endemic over-spending at AIM companies on non-core operations such as financial and professional services.

“Declining profits should mean belt-tightening, but at smaller cap companies overhead costs have gone up 9% in real terms. Many seem to be developing puppy fat, at the expense of profits, when costs could easily be cut from their support costs without reducing the quality of these services.”

SKS Business Services estimates that these companies could reduce their G&A costs by up to 20% per cent just by restructuring their finance function and through a smarter use of outsourcing.

Sanjay Swarup added: “While many of the companies we have looked at are developing reputations for innovation in fields such as biotechnology, oil and gas exploration and technology, many don’t seem to have their eye on controlling their general running costs.”

Sanjay Swarup said: “The absence of MD&A reports and the silence of most companies’ directors on this issue is also worrying. The MD&A report is a great opportunity to provide information to current and potential shareholders. Investors like to hear about profits – both new sources of revenue and also what management is doing to control costs to ensure increased revenue actually boosts profits.”

G&A vs. Revenue Analysis

[i] See chart at the end of this release for summary of SKS’s research into Aim company G&A costs

[ii] The financial reports for financial years-ending 2008-12 (the last full year for which all accounts are available) of 134 randomly selected AIM-listed companies were studied by SKS Business Services in September 2013.

Explore more articles in the Investing category