Top Stories

MIND GAMES: WHAT BEHAVIOURAL FINANCE CAN TEACH YOU ABOUT INVESTING

Published by Gbaf News

Posted on May 5, 2014

5 min readLast updated: January 22, 2026

Published by Gbaf News

Posted on May 5, 2014

5 min readLast updated: January 22, 2026

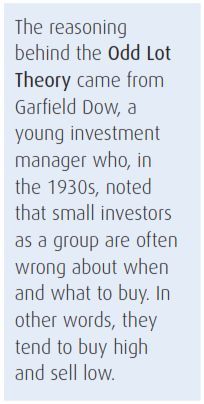

Does it hold true?

Does it hold true?

Of course, individual investors can be successful stock pickers. A recent study conducted by Joshua Coval, a professor at Harvard Business School,concluded that one in five individual investors is able to consistently produce above average equity returns. However, the study also foundthat the vast majority of investors don’t fare as well.

Why do so many individuals under perform the markets over time?

That’s a question that economists and psychologists have been studying for more than three decades. This field of study is called behavioural finance and its goal is to develop a framework to explain why people make the decisions they do about their money. What they’ve discovered is that when it comes to investing, rational choices don’t always apply. What investors know, and what they actually do are often very different.

Mind over money

According to a 2011 study by leading research firm DALBAR, Inc., “Investment results are more dependent on investor behaviour than on fund performance.”

The report also showed that most of this under performance is due to psychological factors that translate into poor timing when it comes to buying and selling investment shares.

So what are these behaviours and what can you do to avoid them?

Consider the following:

Overconfidence

Optimism is a great thing to have in life, assuming it’s grounded in reality. Yet many investors overestimate their ability to beat the market, even when they have failed to do so in the past. Overconfidence can keep investors from meeting their goals because they may save or invest too little if they overestimate returns. It can also keep them from learning from their mistakes.

Rather than letting overconfidence derail your long-term plans, experts suggest taking a steadier route to building financial security by adopting a consistent monthly investment plan. Although dollar cost averaging doesn’t guarantee a profit and can’t protect against loss in a declining market, it can help you ease into the market, buying more shares when prices are lower and fewer shares when prices are high. Over time, this can help lower the total average cost per share you pay for your investments.

Herd behaviour

Herd behaviour

Remember the dotcom bubble of the late 1990s, early 2000s? Like many investing fads, the driving force behind this behaviour is the tendency for individuals to mimic the actions (rational or irrational) of a larger group. But as so many investors painfully learned, chasing the herd can be risky. That’s because focusing on short-term performance can hinder your potential long-term success. The lesson here? Before you jump on the bandwagon, do your homework and remember: Past performance does not guarantee future returns. Understanding what you’re buying and why is essential to making the right decisions for your unique circumstances and long-term investment goals.

Loss aversion

Behavioural finance teaches us that as investors, we tend to value gains and losses differently. In fact, some studies suggest that people feel a decline in the value of their investments twice as keenly as they do an increase of the same value. As a result, many investors are more willing to sell their winners than they are to dump a losing investment.

If you recognize loss aversion as part of your behaviour, how do you overcome it? Start by (a) building a broadly diversified mix of investments to help soften the impact of market volatility on your overall portfolio;(b) rebalancing your investments on a regular basis to ensure your portfolio is right for your particular goals, risk tolerance and time frame; and(c) keeping your focus on your overall progress, not the short-term ups and downs of your portfolio.

Anchoring

Behaviourists have demonstrated that when it comes to making investment decisions, most people are strongly affected by “anchors,” or points of reference, that may or may not be relevant to the decision at hand. In other words, they tend to embrace information that supports their view rather than seeking information that contradicts it.

What’s next

What’s next

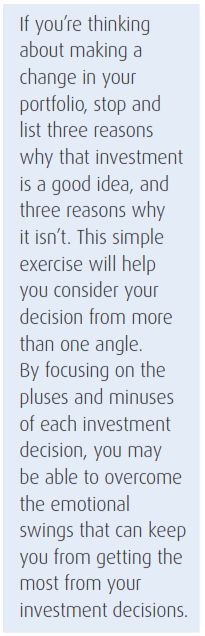

The next time you think you have the market figured out, or you think you’ve spotted a portfolio manager who is on a winning streak, step back and look more closely. Are you seeing the markets through your own lens of hopes and projections or are you making decisions based on fundamentals and facts? Remember, successful investors base their decisions on a variety of inputs in order to gain the truest picture possible of an investment’s prospects.

BMO Financial Group provides this publication to clients for informational purposes only. The information herein reflects information available at the date hereof. It is based on sources that we believe to be reliable, but is not guaranteed by us, may be incomplete, or may change without notice.

It is intended as advice of a general nature and is not to be construed as specific advice to any particular person nor with respect to any specific risk or insurance product. Comments included in this publication are not intended to be legal advice or a definitive analysis of tax applicability or trusts and estates law. Such comments are general in nature for illustrative purposes only. Professional advice regarding an individual’s particular position should be obtained. You should consult an independent insurance broker or advisor of your own choice for advice on your insurance needs, and seek independent legal and/or tax advice on your personal circumstances.

BMO Nesbitt Burns Inc. and BMO InvestorLine Inc. are wholly owned subsidiaries of Bank of Montreal and Members of the Canadian

Investor Protection Fund and IIROC.

® “BMO (M-bar roundel symbol)” is a registered trade-mark of Bank of Montreal, used under licence.

For more information please visit www.bmo.com/wealthmanagement

Explore more articles in the Top Stories category